BRIDS Market Pulse

|

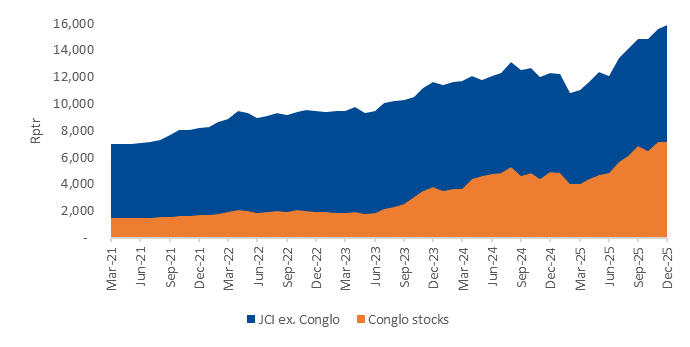

Chart of the week – JCI Market Cap Conglo vs. Ex-Conglo |

|

|

Source: Bloomberg, BRIDS Estimates |

In the spotlight

- JCI corrected -0.6% w-w but foreign fund inflow sustained

- JCI’s correction was driven primarily by declines in conglo names (e.g., BREN, CUAN, BRPT, BUMI, DEWA), alongside noticeably weaker retail liquidity ahead of the holiday season. Meanwhile, large-cap banks (BMRI, BBRI, BBCA) led the gainers following neutral management-change news from the EGM, supported also by newly-listed SUPA.

- Foreign fund flow was maintained at at US$196mn (all market), despite outflows in previous weeks’ momentum names (BUMI, DEWA) and continued outflows in large-cap banks (BBRI). Inflows returned to momentum commodities names (ANTM, UNTR, EMAS), while ASII and BMRI sustained their inflows (9-19 consecutive weeks of inflows for the two names).

- FY26 Market Outlook: we just published our FY26 outlook and set our FY26-end JCI target at 9,440 (bull/ bear case of 9,820/ 9,135). We see the conglo/ momentum theme to prevail in FY26, with 17-32% upside estimated for the stocks under this theme. We see growth recovery to potentially drive valuation re-rating but expect the timing to be gradual. Our sector picks favour Telco, Poultry and Metals on their better growth visibility. We believe the market is pricing in soft growth expectation for Banks and Consumers sectors. Our top stock picks are: BBCA, ISAT, JPFA, ASII, KLBF, AADI, NCKL, ICBP.

- Telco FY26 outlook: Sustained Mobile Momentum and Upside from Fiber Transformation. Our Telco analyst Kafi Ananta expects MNOs to enter a more rational growth phase post-consolidation in FY26, with lower churn following starter-pack rationalization and further ARPU improvement. We expect price-repair efforts to continue through 4Q25-2026F as MNOs shift focus from subs acquisition to renewal monetization. Meanwhile, Indonesia’s MNOs are entering a structural shift toward asset-light models through fiber restructuring. We reiterate Overweight rating on the sector, with top pick on ISAT (Buy, TP Rp3,000).

- Retailers FY26 outlook: Fiscal Boost and Store Expansion as Key Growth Drivers. Our Retail analyst Christy Halim remains bullish on the sector and expect govt fiscal expansion to support a gradual recovery in FY26F. Store expansion remains the growth engine supported by improving purchasing power. We forecast +8.7% yoy sector rev growth with modest margin improvement amid wage inflation & promotions, but productivity gains are likely to lift op margin by 40bps & support +17.5% earnings growth. Maintain Overweight; top picks MIDI, MAPA as we expect gradual FY26F recovery with sector’s val at 10.9x PE FY26F remaining attractive.

- BBNI Nov25 results (bank only): BBNI posted a soft net profit of Rp1.7tr in Nov25 (-4% mom, -3% yoy), as provision reversal offset the spike in other expenses. Opex jumped to Rp3.7tr in Nov25 (+83% mom, +36% yoy), driven by other expenses which doubled yoy and tripled mom. CIR rose to 65.5% as income remained relatively steady. 11M25 net profit of Rp18.6tr (-6% yoy) remained in-line with our and consensus expectations.

- Commodities:

- Coal: Indonesian coal prices remained weak with ICI3 and ICI4 falling to US$61.8 and US$45.9/t respectively on low demand from Chinese buyers and falling domestic prices in China.

… Read More 20251222 BRIDS Market Pulse