BRIDS Market Pulse

In the spotlight

- JCI closed above 9k amid healthy rotation into large-cap banks and metals’ sustained outperformance

- JCI gained 5% w-w and closed above the psychological level of 9k, supported by gains in fundamental stocks TLKM, big-cap banks (BMRI, BBRI, BBNI) as well as conglo DSSA, which offset corrections in conglo groups (BRPT, BUMI, CUAN) and BBCA. Metal sector (+8% w-w) sustained its outperformance, supported by strong nickel and tin prices, followed by Utilities (+6%) and Property (+5%). Consumer, Media and Cigarettes were laggard amid lack of signs of consumers purchasing power recovery.

- A combination of flows into the metal names (INCO, ANTM, MBMA) and large-cap stocks (ASII, TLKM, BBRI) has resulted in inflows of US$249mn, the 15th consecutive week of inflow for JCI. Foreign investors were seen to be sellers in conglo names (BUMI, RAJA, CBDK) and in BBCA.

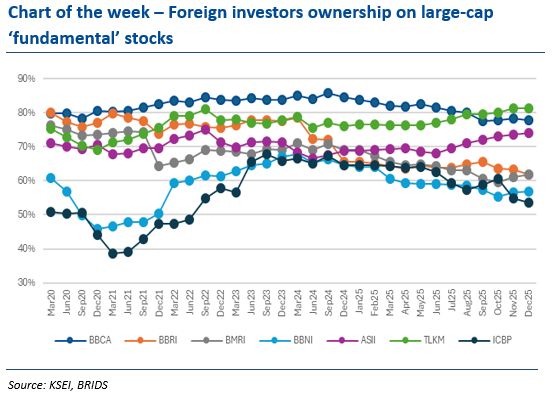

- Investors Dec25 positioning: Based on KSEI data, Domestic funds’ positioning at end of FY25 reflected pessimistic growth expectation, with further trimming in Banks to the lowest positioning in 15 months. Bullish positioning in Metals and select momentum names (BUMI) is also aligned with our market outlook for FY26. Foreign investors’ ownership were maintained at 41.5%, though remaining at historical low level as of Dec25.

- Banking sector FY26 Outlook: K-shape loan growth recovery could weigh on margin and asset quality. Our analyst Victor Stefano maintained Neutral rating on the sector amid potential earnings downside, macro uncertainty, and lingering asset quality risks. We expect positive FY26 earnings growth for banking sector (+5.1% yoy) driven by higher loan growth offsetting the lower NIM in FY26F. However, we opine that NPL could still be in an upcycle in FY26F, with MSME and consumers loan delinquency risks affecting the investment loans.

- ANTM (Buy, TP raised to Rp4,800): Normalizing PTFI supply and support from resilient gold and nickel ore prices. Our analyst Andhika Audrey resumed coverage on ANTM with a positive view on expected gold sales volume normalization in FY26 (~38t), amid expected resumption of PTFI supply and import. Higher nickel ore and gold price anchors our FY26-27 net profit estimates upgrade by 2-16%.

- Commodities:

- Metals: base metals extended their strong performance, with copper (+1% w-w), nickel (+2% w-w), tin (+14% w-w) on the back of tighter supply outlook and restocking activities. Nickel was particularly supported by reaffirmation of Indonesian government’s plan to cut nickel ore production quota to 250-260mn wmt (-30-35% yoy).

- Coal: The positive sentiment due to potential supply cap in nickel also extended into coal, as the government also indicated a plan to cut production quota in FY26. This drove Indonesian thermal coal price to rise with ICI3 and ICI4 up 0.5% and 1.2% to US$61.8/t and US$46.8/t. Recent data showed China’s import rose to record level in Dec25 (58.6Mt, +12% yoy/ +33% mom), likely in anticipation of Indonesia’s production cap policy.

… Read More 20260119 BRIDS Market Pulse