FROM EQUITY RESEARCH DESK

IDEA OF THE DAY

Buana Lintas Lautan: 1Q26: A Transition Quarter; Expect Further Recovery in 2Q26 Onwards (BULL.IJ Rp 272; BUY TP Rp550)

- 1Q26 net profit of US$14mn (+141.6% y-y) came in below estimate at ~12% of FY26F given Aframax settlement lag.

- GPM expanded sharply to 42% (vs 1Q25: 28.2%), driven by structural decline in port charges on longer-haul ME voyages.

- Mgmt. confirm 2Q26F TCE-to-date more than 2x 1Q26 levels; stock pullback offers re-entry ahead of earnings inflection.

To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

RESEARCH COMMENTARY

Macro: BI Delivers Surprise 25bps Hike to 5.50% – Stability Takes Priority

- Bank Indonesia decided to raise the BI Rate by 25bps to 5.50% at its 9 Jun 26 Weekly Board Meeting. The move reinforces BI’s commitment to stabilizing the Rupiah and addressing inflation risks pre-emptively. The Rupiah has weakened by around 8.7% YTD, exceeding BI’s expectations following the May meeting.

- BI also introduced additional support measures, including a 10% reduction in FX hedging swap costs to improve hedging efficiency and reduce carry costs for foreign investors. Meanwhile, repo auction windows across all tenors have been reopened to ensure sufficient liquidity in the money market and banking system, while maintaining double-digit reserve money (M0) growth. BI will also intensify FX and monetary operations, including more frequent SRBI auctions, while strengthening fiscal-monetary coordination, including through government cash placements at BI.

- The latest move resembles BI’s 2018 tightening cycle, when an unscheduled 25bps hike in May was followed by a cumulative 125bps increase through year-end in response to the Fed’s 100bps tightening in 2018. While the Rupiah had weakened by only around 3.5% YTD at that time, it has now depreciated by more than 8% YTD despite contained inflation, highlighting BI’s stronger focus on FX stability and external resilience.

- In our report “After the Hike, What’s Next?”, we identified three conditions that could lead to further BI tightening: persistent Rupiah volatility, inflation above target, and a more hawkish Fed. The current environment already meets two of these conditions, with continued Rupiah weakness and markets increasingly pricing in a Fed rate hike by late 2026 or early 2027, as reflected in elevated UST yields and a stronger USD Index approaching 100.

- Since the previous BI rate hike, the Rupiah has weakened by nearly 500 points toward 18,200, while the 10Y government bond yield rose 40bps to 7.26% a day before the latest inter-meeting hike, broadly in line with our pessimistic scenario.

- Looking ahead, we expect BI to continue relying on market intervention measures, including maintaining attractive yield levels to support capital inflows. Structural efforts to strengthen market confidence remain equally important, we believe, particularly through clearer policy communication and stronger guidance on the broader policy direction. (Bank Indonesia, Economic Research – BRIDS)

MARKET NEWS

MACROECONOMY

China’s Trade Surplus Widened to US$105.4bn in May26

China’s trade surplus widened to US$105.4bn in May 2026 from US$102.7bn a year earlier, exceeding market expectations and marking the largest surplus since January. Export growth accelerated to 19.4% yoy, reaching a record US$376.8bn as firms continued front-loading shipments and inventory accumulation amid concerns over higher energy costs linked to Middle East tensions. Meanwhile, imports rose 27.4% yoy to US$271.4bn, supported by government measures to boost domestic demand. Going forward, stronger import growth suggests improving domestic activity, although external demand remains a key driver of China’s trade performance. (Bloomberg)

SECTOR

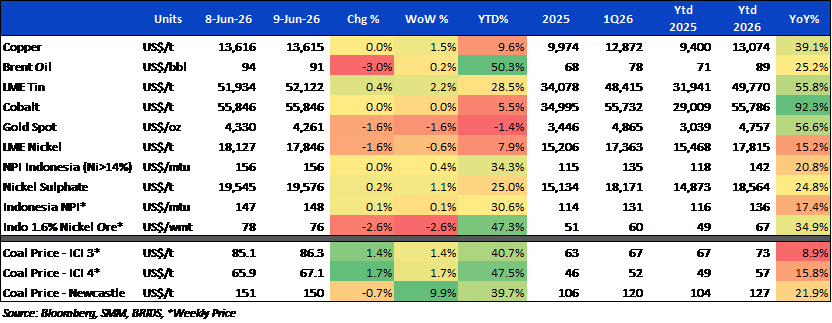

|

Commodity Price Daily Update June 09, 2026 |

Automotive: Indonesia Auto Sales Up 14.0% yoy in May; Retail Sales Rise 16.8% yoy

GAIKINDO reported May 2026 wholesale sales of 69,219 units (+14.0% yoy, -14.3% mom) and retail sales of 71,890 units (+16.8% yoy, -5.1% mom). During 5M26, wholesale and retail sales grew 12.8% yoy and 8.8% yoy to 359,015 units and 369,490 units, respectively. Toyota remained the market leader with 24,846 wholesale units sold, followed by Daihatsu (11,140 units), Suzuki (6,108 units), and Mitsubishi Motors (4,166 units). Notably, Chinese automaker Jaecoo entered the top five with 3,000 units sold, highlighting intensifying competition in the domestic auto market. (CNN)

CORPORATE

|

MTDL Approves Rp331bn Dividend MTDL's shareholders approved a cash dividend of Rp331.5bn, equivalent to Rp27 per share (yield: 5.5%), representing a 40.7% payout ratio of its FY25 net profit of Rp813.9bn (+10% yoy). The dividend will be paid on 10 July 2026, with the cum-dividend date set for 22 June 2026. (Emiten News)

MIKA Declares Rp43/share Dividend MIKA announced a cash dividend of Rp43/share (2.8% yield), as approved by shareholders at the AGMS on 9 June 2026. The dividend represents a payout ratio of approximately 43.8% of the company’s FY25 net income. (Company)

TBIG Declares Rp1.05tr Dividend TBIG shareholders approved a cash dividend of Rp1.05tr, equivalent to Rp47/share (yield: 3.1%), at the company's AGMS on 9 June 2026. The dividend represents approximately 74% of FY25 net profit and will be distributed on 9 July 2026 to shareholders recorded on the 22 June 2026 recording date. (Kontan)

TBIG Allocates Rp4tr Capex for Tower and Fiber Expansion TBIG plans to allocate Rp4tr in capex for 2026, primarily to support organic growth through new tower construction, fiber optic deployment, and connectivity services based on operator demand. Management remains optimistic that tenancy and tower growth will recover in 2026 as the impact of telecom industry consolidation eases. (Kontan) |