FROM EQUITY RESEARCH DESK

IDEA OF THE DAY

Bank Jago: 3Q24 earnings: Low-risk loans continue to drive growth, offseting lower NIM with lower CoC (ARTO.IJ Rp 2,860; BUY TP Rp 3,900)

- ARTO posted 3Q24 net profit growth (+36% qoq, +71% yoy), driving 9M24 to form 69%/70% of our/cons (in line), driven by lower provision.

- 3Q24 NIM remained under pressure at 6.8% (-54bps qoq) as EA yield fell and CoF increased due to the higher TD portion.

- We raised our LT ROE from 16.7% to 17.1%, as we increased our FY24 loan growth est. to 49.2%. Maintain Buy with a higher TP of Rp3,900.

To see the full version of this report, please click here

AKR Corporindo: Recalibrating our numbers post 3Q24 earnings miss; maintaining recovery expectation in 4Q24E onwards (AKRA.IJ Rp 1,360; BUY TP Rp 1,600)

- We cut our FY24F/FY25F net profit ests. by 15%/8% due to lower distribution margin and lower land sales ASP.

- We believe 3Q24 would be the bottom of AKRA's performance, yet we believe there may still be ~9% cut in cons. est. to meet mgmt. guidance.

- We reiterate our BUY rating with a 6% lower TP of Rp1,600. We expect recovery from 4Q24F onwards from JIIPE and petroleum/chemical vol.

To see the full version of this report, please click here

Japfa Comfeed Indonesia: 3Q24 results: Beating expectations on lower-than-anticipated decline in margin (JPFA.IJ Rp 1,665; BUY TP Rp 2,900)

- Despite delivering lower 3Q24 net profit of Rp617bn (-24% qoq, -28% yoy), JPFA’s 9M24 came in above our/cons. est. (94%/ 95% of FY24F).

- Margin declined as expected, but 3Q24’s gross OPM of 6.2% came in ahead of our 5.6% bullish estimates.

- We raised our FY24-25F net profit est. by 31-26%, rolled forward our valuation to FY25F, and lifted our TP to Rp2,900; maintain BUY rating.

To see the full version of this report, please click here

Macro Strategy: Facing the Headwinds

- The conflation of reflation risk and the depreciation of key DXY basket currencies has sparked market volatility, necessitating caution.

- Various indicators point to strong U.S. economic resilience, which could decelerate the pace of Federal Funds Rate cuts.

- Indonesia's new government has introduced several novel initiatives focused on stimulating growth, though risks to execution remain.

To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

RESEARCH COMMENTARY

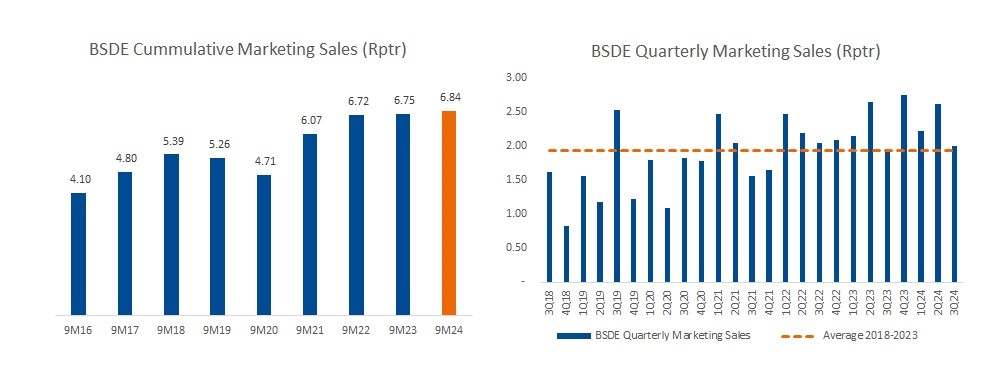

BSDE (Buy, TP: Rp1,550) - Recorded Marketing Sales of Rp6.84tr in 9M24 (72% to our/company's FY24F target)

- BSDE booked marketing sales of Rp2.0tr in 3Q24 (-23%qoq; +2%yoy), bringing its 9M24 achievement to Rp6.84tr (+1%yoy), which reached 72% of our/company's FY24F target of Rp9.5tr, i.e., In-Line.

- The overall 9M24 achievement was aided by the company's key product portfolio in BSD City also new launches in Grand Wisata Bekasi (i.e. Yara at The Kaia- Price Range Rp3.85-7.49bn/unit) and Grandcity Balikpapan (i.e. Townville- Price offered start from Rp2.4bn)

- Overall segment contribution for 9M24 is as follows; Residential 56%, Shophouses 23%, JV Land sales 8%, Apartment 7% and Commercial lots 6%. No significant changes since 2Q24. Relatively in-line with ours. VAT-exempted marketing sales is yet to be disclosed.

- Meanwhile, location-base contribution for 9M24: BSD City 69%, Nava Park 8%, The Zora 7%, Hiera 4%.

- We currently have a Buy rating for BSDE with a TP of Rp1,550 based on our 67% disc.to.RNAV. We believe BSD City’s strong connectivity with Jakarta’s major highways and proximity to transport hubs will remain the key distinctive selling points in the Indonesian property market, allowing BSDE to dominate its market segment by pioneering a well-designed township. (Ismail Fakhri Suweleh – BRIDS)

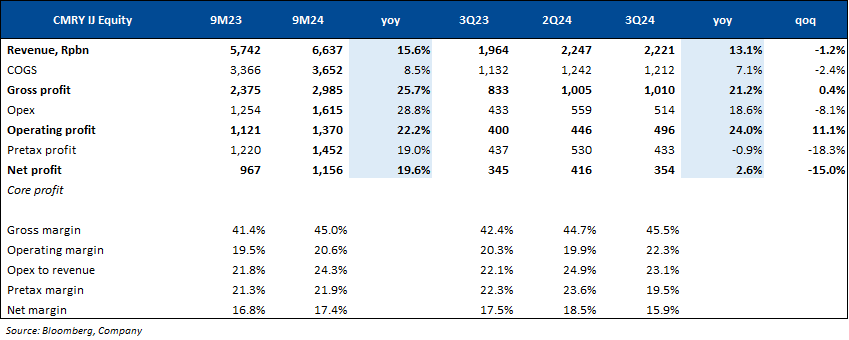

CMRY (Non-Rated) 3Q24 Result

- CMRY reported 3Q24 net profit of Rp353.5bn, +13% yoy (-15%qoq), leading to 9M24 NP of Rp1.16tr, +19.6% yoy and accounted for 77% of consensus’ estimates.

- Solid rev. growth with improved gross margin supported earnings growth. Consumer products reported stronger revenue growth of 21% yoy (3Q24) and 26% yoy (9M24), while Dairy reported 4% yoy rev. growth in 3Q24 and 9M24. (Natalia Sutanto & Sabela Nur Amalina – BRIDS)

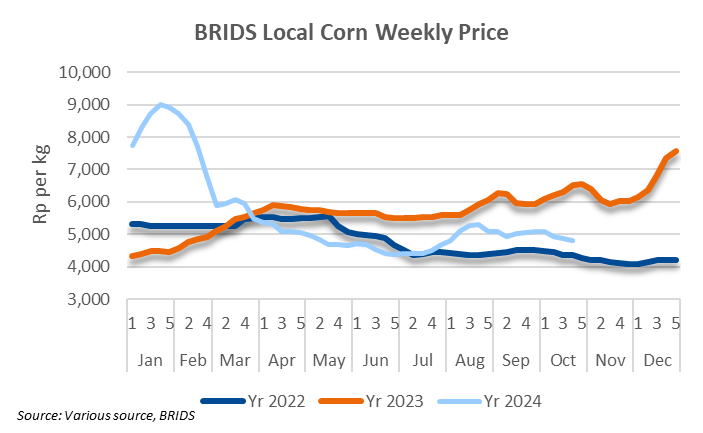

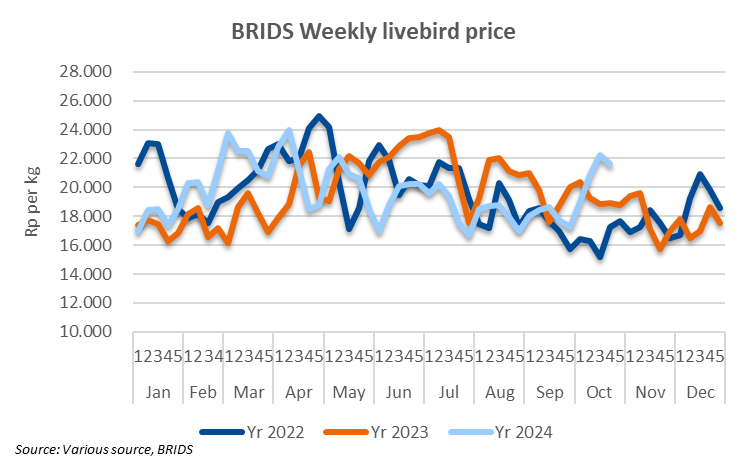

Poultry (Overweight): 4th week of October 2024 Price Update

- Livebird prices have slightly decreased to Rp20.8k/kg, averaging Rp21.6k/kg in the fourth week of October, reflecting a 3% wow decline.

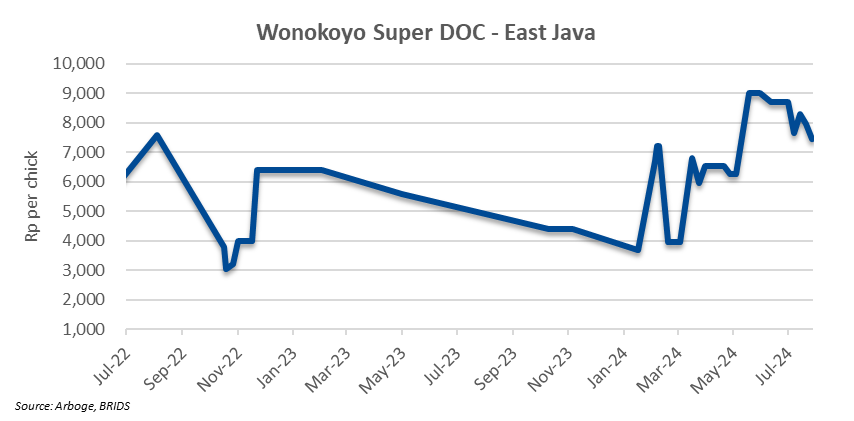

- DOC prices remained stable at around Rp5k/chick.

- Local corn prices have edge down to Rp4.8k/kg, with a weekly average of Rp4.8k/kg in the fourth week of Oct24, marking a 0.9% wow decrease from Rp4.9k/kg in the previous week.

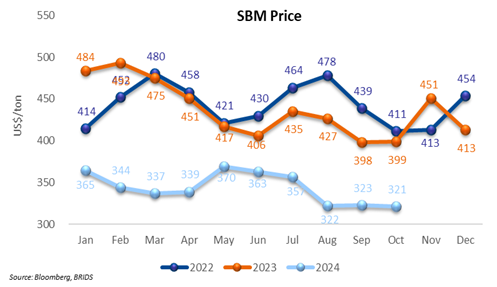

- Soybean meal (SBM) prices fell to an MTD low of US$306/t in the fourth week of Oct24. The average price in Oct24 slightly declined to US$321 (-0.5% mom, -19% you).

- We expect an improvement in earnings for 4Q24, driven by the recovery in livebird prices and controlled increases in feed costs. (Victor Stefano & Wilastita Sofi – BRIDS)

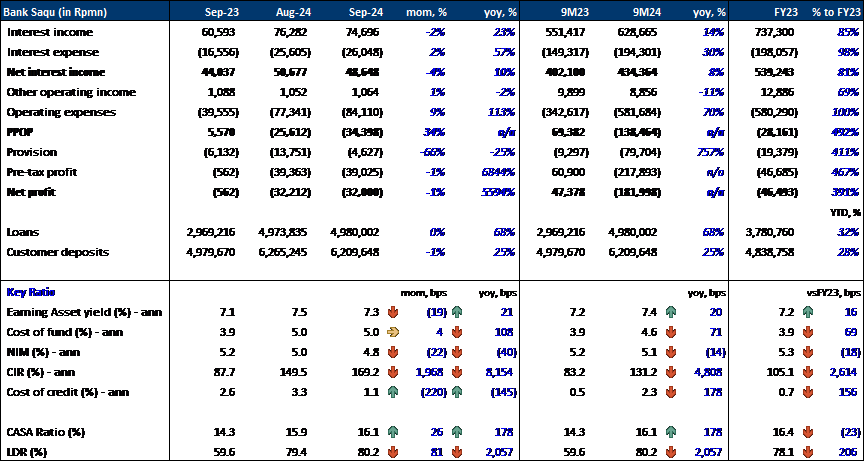

Bank SAQU – Sep24 Results

9M24 Insight:

- Net Loss Due to Elevated Opex: SAQU recorded a net loss of Rp182bn in 9M24, despite generating Rp434bn in NII, as opex totaled Rp582bn.

- CIR and Opex: The CIR reached 131.2% in 9M24, driven by substantial opex, largely attributed to other expenses (Rp250bn) and salary costs (Rp183bn).

- NIM: NIM stood at 5.1% for 9M24, with an EA yield of 7.4% and a CoF of 4.6%.

- Given that SAQU was launched as a digital bank towards the end of FY24, we believe a yoy comparison may not adequately reflect the bank’s performance trajectory.

Sep24 Insight:

- Net Loss: SAQU’s net loss remained unchanged at Rp32bn, as a significant 66% mom drop in provision expenses was able to offset the 34% lower PPOP.

- CIR: CIR rose to 169.2% in Sep24 from 149.5% in Aug24, as NII fell by 4% mom, while opex increased by 9% mom, largely driven by a 21% mom rise in other expenses.

- NIM: Although CoF remained stable mom at 5.0%, a 19bps decline in EA yield to 7.3% led to a 22bps drop in NIM, bringing it to 4.8% in Sep24. This decline occurred despite an improved LDR of 80.2% (+81bps mom).

- CoC: CoC improved significantly to 1.1% in Sep24 from 3.3% in Aug24.

- Loans and Customer Deposits: Loans and customer deposits remained steady at Rp5.0tr (flat mom) and Rp6.2tr (-1% mom), respectively, resulting in an LDR of 80.2% (+81bps mom). The CASA ratio improved slightly to 16.1% (+26bps mom).

Summary:

- Overall Performance: In our view, the bank’s performance continues to reflect the costs associated with its developmental stage, requiring substantial investment in promotional activities, which have significantly driven up opex. We also note that the bank’s loans have stagnated at c. Rp5tr over the past 3 months, which is unusual given its early stage of development. (Victor Stefano & Naura Reyhan Muchlis – BRIDS)

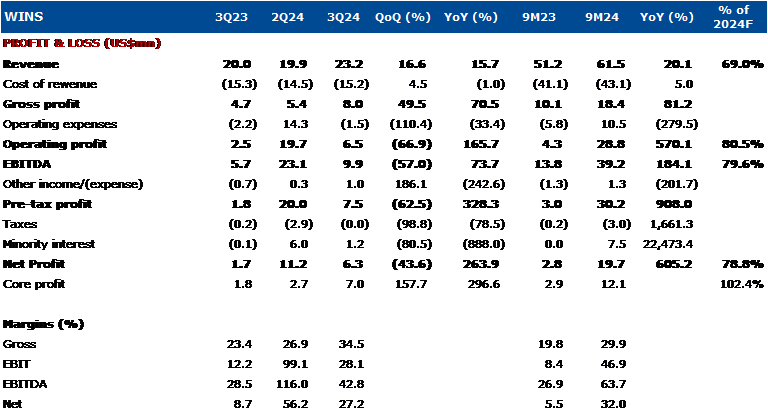

WINS (Buy, TP: Rp760) 3Q24: Better than expected

- 3Q Rev grew to US$23.2mn, +16.6% qoq,+15.7% yoy, reaching 69%/71% of our/cons estimate

- 3Q core profit reached US$7mn, +158% qoq, reaching 102%/93% of our/cons estimate.

- We believe the strong outperformance was supported by higher charter rates on high-tier and med-tier vessels, along with improved utilization rate from its latest AWB (Thailand), and new LT contracts for 2 of its PSV. (Timothy Wijaya – BRIDS)

MARKET NEWS

SECTOR

Commodity Price Daily Update Oct 28, 2024

Automotive Manufacturers Capitalize on Electric Car Import Incentives with Production Commitment

Several automakers are leveraging Indonesia’s CBU electric vehicle import tax and luxury tax exemptions under Ministerial Regulation No. 6 of 2023, derived from Presidential Regulation No. 79 of 2023, by committing to local production. Aion Indonesia has secured these incentives for three models, pledging a plant in Cikampek, West Java, to produce 50,000 units annually starting 1Q25. Citroen Indonesia has also used the incentives for 4,500 units of its E-C3 model, backed by a bank guarantee matching the government’s incentive amount. (Kontan)

Heavy Equipment: National Production Aims for 8,000 Units Amid Import Issues

Indonesia’s heavy equipment sector is gradually recovering with rising demand, despite ongoing import hurdles. The Indonesian Heavy Equipment Industry Association (Hinabi) reported production at 5,138 units as of 9M24, decline 18% yoy. However, 3Q24 production rose by 10% qoq, driven by mining and plantation needs. Hinabi remains confident in hitting the 8,000-unit target for 2024, though import restrictions still affect component availability. (Kontan)

Telco: APJII Urges New Government to Prioritize Digital Infrastructure in Remote Areas

The Chairman of the Indonesian Internet Service Providers Association (APJII) urged the new government to prioritize the development of digital infrastructure in remote areas. According to APJII, over the next five years, the new goverment should aim for internet penetration of up to 95%, especially in rural areas and regions designated as 3T (underdeveloped, remote, and border areas). (Investor Daily)

Comment: Based on latest 2024 APJII, Indonesian internet penetration only grew to 79.5% +131bps yoy to 221.6mn internet users in FY24 vs (215.6/210.0mn in FY23/FY22). Hence, govt should steer policies towards further user penetration to 95%. Govt. will have to balance the pros and cons of enhanced satellite coverage for 3T areas and increasing the cellular coverage further. (Niko Margaronis – BRIDS)

CORPORATE

ANTM Partners with PLN to Power Kolaka Smelter with Cleaner Energy

ANTM has partnered with PT PLN (Persero) to supply 150 MVA of electricity to its Ferronickel Smelter in Pomalaa, Southeast Sulawesi. This shift to PLN’s electricity will enable ANTM to reduce reliance on fossil fuel power, aligning with its commitment to environmental sustainability and national decarbonization goals. Managed by ANTM’s Nickel Mining Business Unit, the smelter, with an annual capacity of 27,000 tons of nickel in ferronickel (TNi), aims to enhance operational efficiency to meet predominantly export-driven market demand. (Company)

BRMS Gold Production Reached 45,366 oz by 3Q24

BRMS recorded rapid growth in its gold production in 3Q24, driven in part by the strong performance of its gold plant in Palu. BRMS reported gold production of 45,366 oz by 3Q24, significantly surpassing its total gold production for 2023 of 23,370 oz. Meanwhile, BRMS's average selling price (ASP) for gold reached US$2,347/oz in 9M24 (2023: US$1,930/oz). (Bisnis)

PTBA Launches Wood Pellet Pilot Plant to Support Energy Transition

PTBA has launched a pilot plant for wood pellets made from Kaliandra Merah in Tanjung Enim, South Sumatra, aimed at producing biomass fuel for coal-fired power plants. This initiative, with a production capacity of 200 kg per hour, continues PTBA’s biomass program started in 2023. The Ministry of Energy and Mineral Resources commended PTBA's carbon management efforts, hoping to inspire further eco-friendly initiatives, as PTBA reinforces its commitment to Indonesia’s 2060 Net Zero Emission target. (Company)

WINS to Distribute FY24 Interim Dividend of Rp34.92bn

WINS announces the distribution of an Interim Dividend of Rp8/share (yield: 1.4%), totaling approximately Rp34.92bn for 4.36mn shares. Approved by the Board of Directors on October 23, 2024, and the Board of Commissioners on October 25, 2024, this dividend is based on the Company’s Comprehensive Income as of 9M24 and will be paid to eligible shareholders. (Company)