FROM EQUITY RESEARCH DESK

IDEA OF THE DAY

Indofood CBP Sukses Makmur: Positive Outlook for FY24-25F Intact with Potential Boost from Festive Season Demand (ICBP.IJ Rp 12,150; BUY TP Rp 14,000)

- Following the solid 9M24 results, we raise our FY24-25F revenue growth forecast to 8% yoy, primarily driven by stronger volume expectation.

- We also expect demand from overseas markets, coupled with stable margins, to support FY24/25F core profit growth of 7%/11% yoy.

- Maintain Buy rating with a higher TP of Rp14,000. We expect positive momentum to continue into 4Q24 and 1Q25, backed by Eid festivities.

To see the full version of this report, please click here

Indofood Sukses Makmur: CPO price stability and volume growth underpin FY24-25F Outlook (INDF.IJ Rp 7,800; BUY TP Rp 8,800)

- Strong volume growth from ICBP and Bogasari, higher CPO prices, and lower fertilizer costs supported INDF's solid 9M24 performance.

- We project FY24/25F core profit growth of 5.8% and 9.3% yoy, driven by ICBP and robust performance in the agribusiness division.

- We expect INDF will benefit from lower fertilizer costs until 1H25. We maintain a Buy rating with a higher TP of Rp8,800 (FY25F PE of 6.6x).

To see the full version of this report, please click here

Sarana Menara Nusantara: Well-positioned for Further Inorganic Growth Amid Strong EBITDA Deliveries in 9M24 (TOWR.IJ Rp 770; BUY TP Rp 1,400)

- 9M24 earnings were broadly in line driven by strong non-tower revenue growth (+28.1% yoy) and high capex, leading to elevated D&A and OPEX.

- We expect the upcoming RI to improve the earnings outlook, while the stronger 3Q24 EBITDA improves headroom for more acquisitions.

- Maintain Buy rating with an unchanged TP of Rp1,400 on TOWR’s strong positioning and attractive valuation.

To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

RESEARCH COMMENTARY

BRIS (Hold, TP: Rp3,000) - 3Q24 Concall KTA

Hajj Savings Program and Account Growth Strategies:

- Initial Capital and Lock-in Incentive: The incentive proposes that customers deposit Rp25mn in a long-term, 0% interest lock-in account, where funds remain until required, akin to a 20–25-year time deposit. This arrangement benefits the bank by creating a steady fund base without the financial cost of interest.

- Augmenting Account Balances: By holding funds in the bank’s records, it becomes easier for customers to meet future Hajj payment requirements or cover any subsidy shortfall, effectively driving customers to increase their balances over time. The program development is also still ongoing.

- Retention and Product Stickiness: Customers tend to remain loyal to the bank where they initially opened their Hajj savings accounts, presenting a valuable opportunity for cross-selling additional products beyond Hajj-related services.

Cross-Selling Mechanisms for Hajj Savings Customers:

- Challenges in Cross-Selling Awareness: Branch representatives often perceive Hajj savings customers as ‘idle’ once their balance reaches Rp25mn. This underutilization stems from a lack of training on the potential to upsell and manage these clients actively.

- Enhancing Sales Skills: Efforts are underway to address this through training at branch levels, enabling RMs to function as ‘portfolio managers’ capable of offering a broader range of products, including multipurpose loans, mortgages, automotive financing, and even gold installment plans.

- Data-Driven Selling: A new dashboard called "Dataku" is being developed to provide RMs with customer insights for more targeted offers. There are also pre-approved lending limits for payroll customers, which accelerates the application and approval process for various loan products.

Gold Business Expansion and Partnership:

- Focus on Gold Installments: Initially, BRIS’ gold business model was heavily focused on gold pawning. However, now the bank focuses more on gold installments rather than gold pawning, as installment plans reduce costs associated with appraisal fees and provide easier customer access. BRIS’ gold business composition was almost at 50:50 in 9M24.

- Educating Customers on Gold Investments: BRIS aims to educate customers on investment, especially gold, which is more accessible and understandable than other investment products like mutual funds or insurance-linked products.

- Partnership with Gold Suppliers: BRIS is exploring partnerships with various gold suppliers, such as ANTM and HRTA, to meet the rising demand for gold installments.

Development and Integration of a Super App:

- Features and Functionalities: The super app allows customers to check balances quickly, explore investment options such as mutual funds, and open Hajj accounts with ease, among other enhancements.

- Increased Customer Retention and CASA: By simplifying transaction processes and drawing inspiration from leading super apps, the bank hopes to increase customer engagement, thereby boosting CASA balances and overall retention rates.

Impact of Indonesian Islamic Banking Development on BRIS’ Competitive Position:

- Advantage from Scale and Branch Network: BRIS, which resulted from the merger between BMRI's, BBNI's, and BBRI's sharia businesses positions it as the fifth largest branch network in Indonesia. This extensive reach builds trust among customers who value physical presence and ATM availability.

- Government Support and Competitive Edge: BRIS benefits from lower reserve requirements compared to conventional banks, offering a slight advantage.

- Public Awareness and Brand Positioning: Increasing brand recognition remains a priority, as public awareness of BRIS still lags behind the big 4 banks. Strategic investments in branches, ATMs, and marketing are anticipated to improve visibility and credibility.

Investment and Infrastructure Cost Considerations:

- Return on Investment Strategy: In the short term, the bank aims to keep CIR at 45-47%. Over time, management expects enhanced revenue from fee-based services and efficient asset management to help lower CIR further, ideally in the low 40%s.

- Super App and Brand Awareness Initiatives: The upcoming launch of the super app is also part of a broader strategy to boost brand recognition and engagement, further aiding in long-term cost reductions through higher customer retention and streamlined digital operations. (Victor Stefano & Naura Reyhan Muchlis - BRIDS)

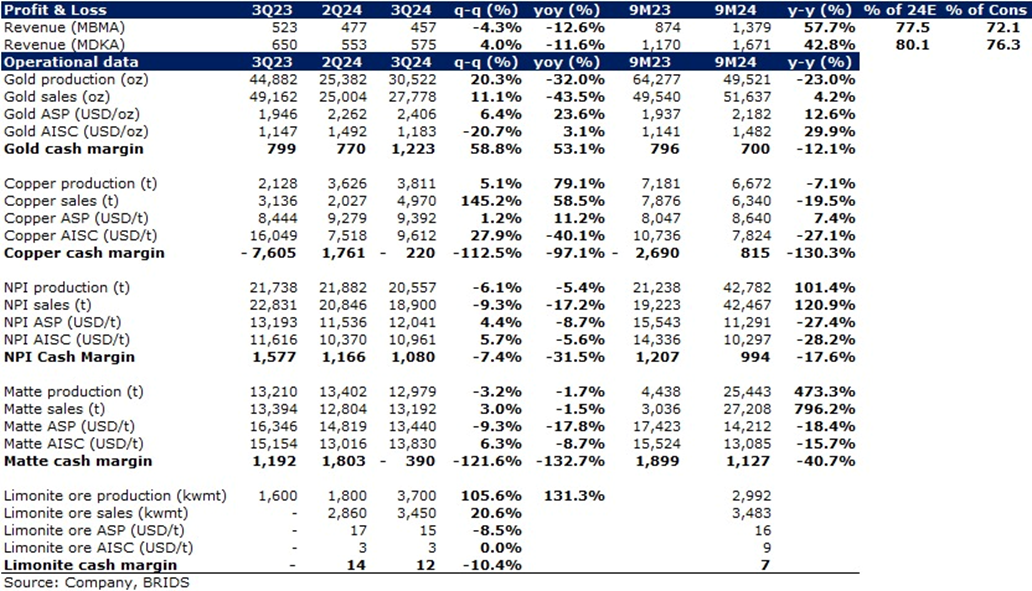

MDKA (BUY, TP: Rp3,000) & MBMA (BUY, TP: Rp650) 3Q operational figures: below expectation

- Gold: Gold segment was the top performer in 3Q with an increase in sales of +11%, ASP +6%, and lower AISC -21% qoq. Consequently, cash margin grew significantly to US$1,223/Oz, +59% qoq.

- Copper: Copper saw a much-improved sales +145% qoq with flattish ASP +1.2%. However, AISC blew up +28% qoq to US$9.6k/t which ultimately brought cash margin to a negative of -US$220/ton

- NPI: Sales and production declined -6%/-9% as expected from the maintenance of BSI smelter. Meanwhile, AISC grew stronger than ASP which resulted in a weaker cash margin of US$1,080/ton, -7.4% qoq

- Matte: Nickel matte ASP declined -9% due to the weaker LME price. AISC grew +6% due to higher NPI price. Thus, Matte declined to negative cash margin territory of -US$390/ton

- Looking at the segments where only Gold's cash margin improved qoq, we expect another margin shrinkage in 3Q24 with possible net loss in MDKA. (Timothy Wijaya – BRIDS)

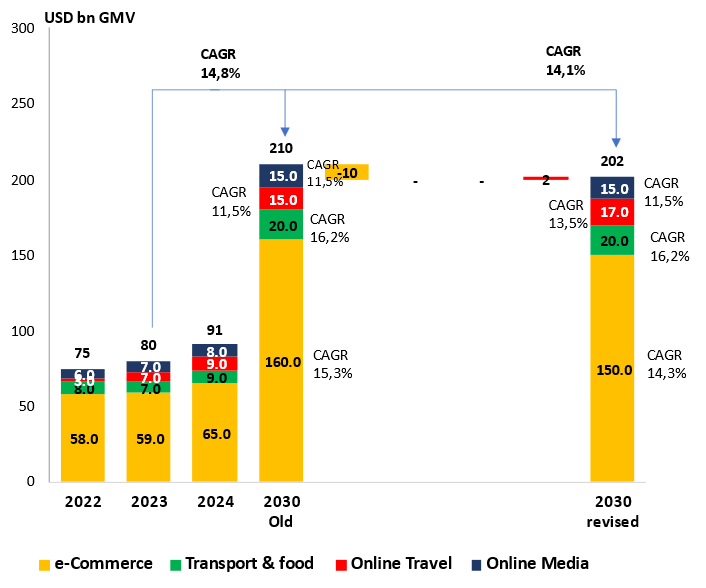

Technology Update: Indonesia - GMV e-Conomy SEA 2024 Analysis

Key Drivers:

- E-commerce:

Indonesia’s e-commerce GMV is expected to grow from US$59bn in 2023 to US$150bn in 2030 (revised) with a CAGR of 14.3%. This growth is driven by the continued expansion of online shopping, evidenced by the acquisition of a local e-commerce platform by a leading social media company to reassess and strengthen growth strategies. Moreover, the rising prominence of video commerce has also impacted growth by reshaping the competitive landscape of Indonesia’s e-commerce sector. The capabilities of e-commerce platforms also impact growth.

- Transport & Food:

The GMV of Transport & Food in Indonesia is expected to grow from US$7bn in 2023 to US$20 bn in 2030 (revised) with a CAGR of 16.2%. Expected growth in Transport & Food is supported by the rebound in consumer demand for on-demand services as consumer preference shifts back to dining out while still enjoying the convenience of delivery services. Moreover, companies in this sector in Indonesia are exploring new revenue streams and optimizing operations to enhance profitability in a competitive market.

- Online Travel:

A strong recovery is projected for online travel in Indonesia, with an increase in GMV from US$7bn in 2023 to US$17bn in 2030 (revised) with a CAGR of 13.5%. This is due to significant growth in both domestic and international travel demand. Growth in both travel destinations is also supported by the ability of online travel platforms in Indonesia to offer more comprehensive services and attractive deals to consumers.

- Online Media:

Online Media is expected to grow from US$7bn in 2023 to US$15bn in 2030 (revised) with a CAGR of 11.5%. Key drivers of this expected growth include the increasing consumption of digital content, expansion of video-based platforms, and growth in advertising monetization, which mostly occurs in gaming and video streaming. Moreover, Indonesia is a major hub for mobile gaming, with increased engagement and local developers gaining international recognition. (Niko Margaronis – BRIDS)

MARKET NEWS

MACROECONOMY

Trump has Won the Presidential Election

Trump has won the presidential election. Trump sweep the swing state, winning back the Pennsylvania, Wisconsin, and Georgia. Republican has also won the senate, while House majority remain unclear as of this writing. Market reaction was as expected, reflecting the 2016 movement. UST and DXY jumped while US Indexes reached all-time highs. (Various)

SECTOR

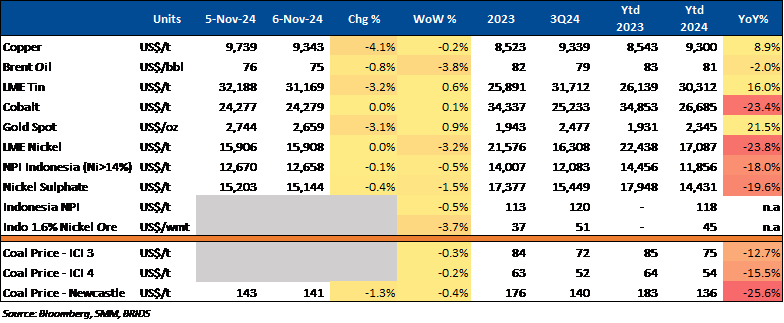

Commodity Price Daily Update Nov 6, 2024

CORPORATE

Apple Plans to Build a Factory to Comply with TKDN (Domestic Component Level) Requirements

Apple has submitted an investment plan of nearly US$10mn to boost production in Indonesia. The company plans to invest in a factory in Bandung, located southeast of Jakarta. This plant will be developed in collaboration with several existing suppliers within Apple's network. This move comes as part of the tech giant's efforts to lift the sales ban on the iPhone 16 in the domestic market. (Kontan)

ISAT Partners with Ericsson to Launch Full-Stack Digital Monetization Platform

ISAT Partners with Ericsson to Introduce the World’s First Full-Stack Digital Monetization Platform. According to ISAT, this partnership is a concrete effort to deliver a marvelous experience through digital services with real-time monetization and an adaptive platform. (Investor Daily)

KLBF to Boost Local Vaccine Production

KLBF plans to enhance local vaccine production over the next five years through PT Kalventis Sinergi Farma, aiming to meet Local Content Requirements (TKDN) and explore export opportunities. While capital expenditure details remain undisclosed, KLBF ensures vaccine availability for all age groups. (Kontan)

PHE Achieves 1.04 MBOEPD as of 3Q24

PT Pertamina Hulu Energi (PHE) recorded oil and gas production of 1.04mn barrels of oil equivalent per day (MBOEPD) as of 3Q24. This production achievement consists of 554,000 barrels of oil per day (MBOPD) and 2.84bn standard cubic feet per day (BSCFD) of gas. By the end of 3Q24, PHE also successfully completed drilling activities on 13 exploration wells, 585 development wells, 769 workover wells, and 26,928 well services. (Kontan)

SCMA to Distribute Interim Dividend of Rp316.84bn

SCMA will distribute an interim dividend of Rp316.84bn, or Rp5/share (yield: 3.9%), following board approval on 4th Nov24. This marks the first interim dividend since 2019 when SCMA paid Rp25/share. As of 9M24, SCMA’s net profit surged 115.28% yoy to Rp509.24bn. (Kontan)

Telkomsel Launches Mola Golf & Mola Sport on IndiHome TV

Telkomsel, in partnership with Mola TV, has launched Mola Golf and Mola Sport channels on IndiHome TV, featuring exclusive broadcasts of global sports events. Management highlighted this move as part of Telkomsel’s commitment to empowering communities through innovative digital solutions. (CNBC)

TPIA Prepares Funds for Maturing Bonds

TPIA has allocated Rp229.75bn to settle its Sustainable Bonds I Phase I Year 2017 Series C, maturing on 12th Dec24. Mgmt. stated that the principal and final coupon payment will be made to PT Kustodian Sentral Efek Indonesia (KSEI) in accordance with applicable regulations. (Eiten News)