FROM EQUITY RESEARCH DESK

IDEA OF THE DAY

Banks: Might Not Be the Best Time but Should Not Be the Worst (OVERWEIGHT)

- At > -3SD of its 5-year mean, we believe current valuations have priced in excessive risk premium and negative growth.

- Amid underperformance compared to peers, BBCA is the safest bet based on our analysis under current situation.

- Despite lingering uncertainties, we upgraded our sector rating to Overweight, with BBCA as our top pick.

To see the full version of this report, please click here

Metal Mining: Moderating Regulatory Risks (OVERWEIGHT)

- We believe the regulatory risks for the sector are moderating as the punitive proposals are becoming more accommodative.

- Single-SOE exporter (DSI) remains a key overhang as goods ownership, pricing, settlement and implementation remain unclear.

- We prefer ANTM and TINS, given limited exposure to DSI, resilient demand drivers, and improving earnings visibility.

To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

MARKET NEWS

MACROECONOMY

China’s Inflation Remained Subdued at 1.2% yoy in May26

China’s inflation remained subdued at 1.2% yoy in May 2026, unchanged from April and slightly below market expectations, highlighting the continued absence of broad-based price pressures. Higher transportation costs, driven by elevated energy prices and supply-chain disruptions linked to Middle East tensions, helped offset persistent weakness in food prices, which declined 1.7% yoy amid falling pork and fruit prices. Meanwhile, core inflation eased slightly to 1.1% YoY from 1.2%, while consumer prices edged down 0.1% mom, underscoring a still-fragile domestic demand environment despite rising external cost pressures. (Bloomberg, CNBC)

Indonesia’s Consumer Confidence Index Declined to 120.9 in May26

Indonesia’s Consumer Confidence Index declined to 120.9 in May 2026 from 123.0 in April, lowest since September 2025. The moderation was mainly driven by a weaker assessment of current economic conditions, with the current economic condition index falling 4.3 points to 112.2 while durable goods purchases declined 4.3 points to 108.3. Perceptions of job availability over the past six months dropped 3.8 points to 105.0 while expectations for eased slightly by 0.4 points to 136.5. Moreover, expectations for job availability and business activity improved modestly, with both indices rising 0.4 points to 128.1 and 124.5. Overall, consumer confidence remained firmly above the 100-point optimism threshold. (Bank Indonesia)

US Headline Inflation is Projected to Accelerate to 4.2% yoy in May26

US headline inflation is projected to accelerate to 4.2% YoY in May 2026 from 3.8% in April, marking the highest reading since April 2023 and the third consecutive monthly increase. The pickup is largely attributed to higher gasoline prices following the Iran-related energy shock, although broader inflation pass-through remains limited. On a monthly basis, CPI is expected to rise 0.5%, slightly below April’s 0.6% increase. Meanwhile, core inflation is forecast to edge up to 2.9% YoY from 2.8%, while monthly core CPI is expected to moderate to 0.3% from 0.4%, suggesting underlying price pressures remain relatively contained. (U.S. BLS)

US Trade Deficit Narrowed to US$55.9bn in Apr26

The US trade deficit narrowed to USD55.9 billion in April 2026 from a revised USD56.6 billion in March, outperforming market expectations. Exports rose 2.6% to a record USD327.1 billion, supported by stronger shipments of capital goods, industrial supplies, and consumer products, with higher energy exports benefiting from elevated oil prices amid Middle East tensions. Meanwhile, imports increased 2.0% to USD383.0 billion, the highest level in a year, driven primarily by robust demand for capital goods such as computers, semiconductors, and telecommunications equipment, signaling continued business investment momentum. (U.S. BEA)

SECTOR

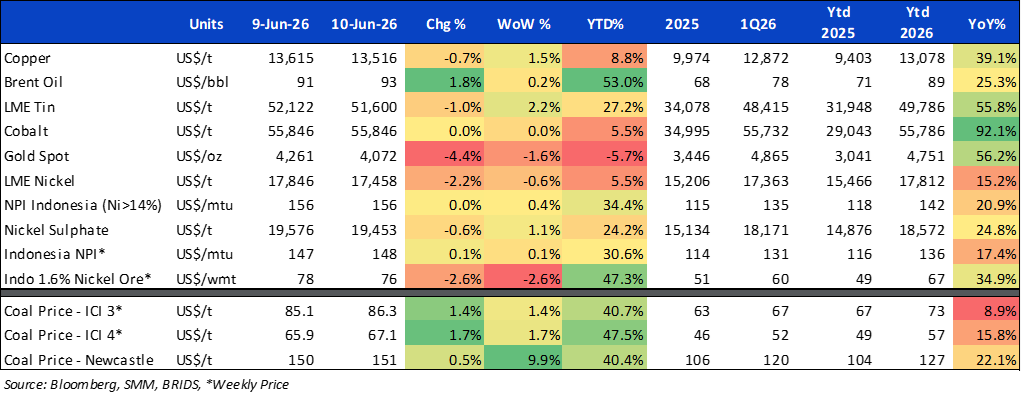

|

Commodity Price Daily Update June 10, 2026 |

CORPORATE

|

ACES Declares Rp548bn Dividend with ACES approved a cash dividend of Rp548.02bn, equivalent to Rp32.01/share (9.2% yield), representing approximately 82% of FY25 net profit of Rp668.73bn. The dividend payment is scheduled for 10 July 2026. (Emiten News)

ANTM Declares Rp5.05tr Dividend ANTM shareholders approved a FY25 cash dividend of Rp5.05tr, equivalent to Rp210/share (7.6% yield), at the company's AGMS on 10 June 2026. The dividend represents a 70% payout ratio, lower than the 100% payout ratio distributed for FY24 earnings. (Kontan)

MIDI Reports Strong Post-Eid Sales Momentum MIDI reported strong post-Eid sales performance, with Alfamidi’s MTD May26 SSSG reaching +7.15% yoy, while MTD Apr26 SSSG improved to +1.12% yoy from -14.77% in MTD Apr25. Management remains confident in achieving its FY26 guidance of mid-single-digit SSSG growth. (Company)

OMED Declares Rp110bn Dividend |

OMED approved a final cash dividend of Rp4.08/share (2.1% yield) from FY25 earnings. The total dividend allocation amounts to approximately Rp110.4bn. (Kontan)