|

FROM EQUITY RESEARCH DESK |

|

|||||||||||

|

IDEA OF THE DAY |

|

|

|

|

|

|

||||||

|

Midi Utama Indonesia: Operational Recovery Continues in 4Q25 and Jan26 (MIDI.IJ Rp354; BUY TP Rp550) · MIDI’s operational performance indicates improvement, with SSSG turning positive at end-FY25 and reaching mid-single digit in early Jan26. · We adjusted down SSSG & store expansion assumptions but still expect MIDI to deliver solid +9.4% rev & +16.8% earnings growth in FY26F. · We reiterate Buy rating with an unchanged TP of Rp550; current 14.1x FY26F PE is attractive given the potential growth prospects. To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

MARKET NEWS |

||||||||||||

MACROECONOMY

|

Bank Indonesia Kept Its Policy Rate at 4.75% at the Jan26 Bank Indonesia (BI) kept its policy rate at 4.75% at the January 2026 Governor’s Meeting, maintaining its focus on Rupiah stability amid heightened global uncertainty while continuing to support economic growth. BI’s Governor stated that the recent Rupiah depreciation reflects both global factors and domestic perceptions, including concerns related to fiscal discipline, the ongoing Deputy Governor nomination process, and rising foreign exchange demand from SOEs for operational purposes. In this regard, BI reaffirmed its commitment to exchange-rate stabilization through its triple intervention, as well as to maintaining strong independence and governance. (Bank Indonesia)

Indonesia’s Loan Growth Picked Up to 9.69% yoy in Dec25 Indonesia’s loan growth picked up to 9.69% yoy in Dec25, from 7.74% in November, marking the strongest expansion since February, supported by government efforts to stimulate domestic demand. Credit growth was driven by investment loans (21.06%), consumption loans (6.58%), and working capital loans (4.52%). Nevertheless, undisbursed credit facilities remained sizable at Rp2,439.2tr, or 22.12% of total approved credit ceilings. (Bank Indonesia) |

SECTOR

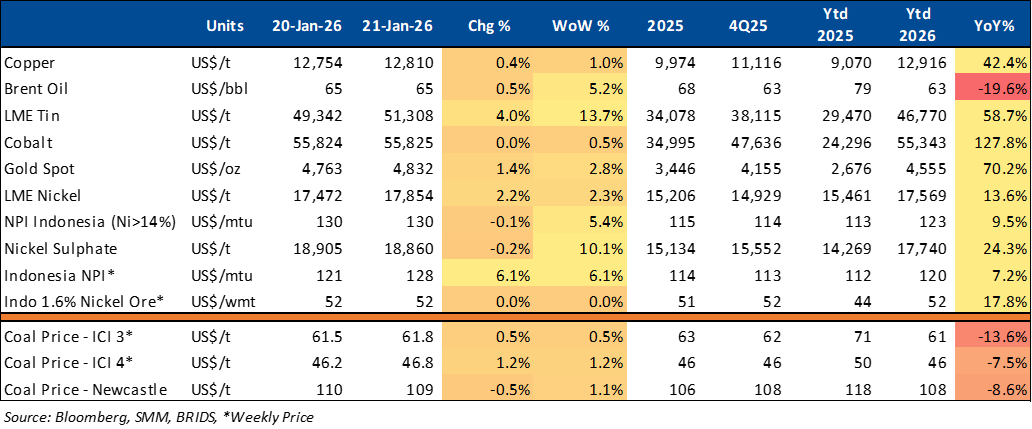

Commodity Price Daily Update Jan 21, 2026

CORPORATE

AVIA to Operate New Paint Factory in Mid-2026

AVIA plans to start operating a new paint factory in Cirebon, West Java, by mid-2026 to support long-term growth. The plant, with total capex of Rp750bn, will initially run at 80,000–100,000 metric tons capacity, expandable to 200,000 metric tons. The facility is expected to strengthen production capacity, especially for wall paint, while improving efficiency and product quality, supported by AVIA’s extensive nationwide distribution network. (Kontan)

BUMI Sees Major Share Sell-Down by Two Key Investors

BUMI shares came under the spotlight after two major investors divested significant stakes in the company. Treasure Global Investments Limited (TGIL), an affiliate of the Salim Group, sold 18.19bn BUMI shares for a total value of Rp6.91tr. Earlier, China Investment Corporation (CIC), through its subsidiary Chengdong Investment Corporation, had also offloaded 3.71bn BUMI shares worth Rp1.32tr. TGIL stated that the divestment was carried out as part of a shareholder restructuring process. (InvestorDaily)

CMRY Establishes New Subsidiary PT Artha Rasa Cimory

CMRY has established a new subsidiary, PT Artha Rasa Cimory (ARC), domiciled in West Jakarta. ARC has an authorized capital of Rp10bn, with Rp2.5bn paid-up capital. CMRY holds a 99% stake, while 1% is owned by Farell Grandisuri. The establishment, effective January 2026, aims to support CMRY’s long-term business plans and is not expected to have any negative impact on operations or financial condition. (Emiten News)