|

FROM EQUITY RESEARCH DESK |

|

|||||||||||

|

IDEA OF THE DAY |

|

|

|

|

|

|

||||||

|

Bank Tabungan Negara: FY25 Results: Beating estimates on strong NIM amid EIR adjustments and improving CoF (BBTN.IJ Rp1,345; BUY TP Rp1,500) · BBTN booked NP of Rp1.2tr in 4Q25 (doubled qoq, +30% yoy) resulting in FY25 NP of Rp3.5tr (+16% yoy), beating our and consensus’ FY25F. · NIM was robust at 4.2% in 4Q25 as EA yield increased supported by EIR adjustment and CoF improvement, offsetting higher CoC. · Maintain a Buy rating with a higher TP of Rp1,500 as we adjusted FY26/27F earnings by +9/+3%. To see the full version of this report, please click here

Bank BTPN Syariah: FY25 Results: Missing Estimates on Elevated CoC Due to One-off (BTPS.IJ Rp1,225; BUY TP Rp1,400) · BTPS posted 4Q25 net profit of Rp255bn, bringing FY25 NP to Rp1.2tr (+13% yoy), below our/cons ests. on higher opex and 4Q25 CoC. · Mgmt guides for positive loan growth in FY26F and net profit to grow in high single digit, supported by lower CoC despite a higher CIR. · Maintain a Buy rating with a lower TP of Rp1,400 based on 2-year avg. CoE of 12.9% and FY26F RoE of 13.2%, implying FV PBV of 1.0x. To see the full version of this report, please click here

Indosat Ooredoo Hutchison: Solid Mobile; Potential Div Upside from Fiber Sale (ISAT.IJ Rp2,210; BUY TP Rp3,000) · 4Q25 ARPU reached Rp44k (+10% qoq), with traffic remaining the key driver (+7.5% qoq), supported by AI-driven hyper-personalization. · FY26F capex is guided at Rp13tr, excluding spectrum license costs, while management aims to secure both 700MHz and 2.6GHz bands. · We maintain Buy rating and TP Rp3,000, supported by solid mobile while net FiberCo proceeds (US$560mn) could provide dividend upside. To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

MARKET NEWS |

||||||||||||

MACROECONOMY

|

US Non-farm Payrolls Rose 130K in Jan26 US non-farm payrolls rose 130K in January 2026, beating expectations and rebounding from a revised 48K in December, while the unemployment rate edged down to 4.3% from 4.4%, signaling a stable labor market. Job gains were led by health care, social assistance, and construction, while federal government and financial sector jobs declined. Labor force participation improved to 62.5% and U-6 unemployment fell to 8.0%. However, 2025 job growth was sharply revised lower to an average 15K per month, signalling weaker underlying labor conditions. (U.S. BLS, Bloomberg) |

SECTOR

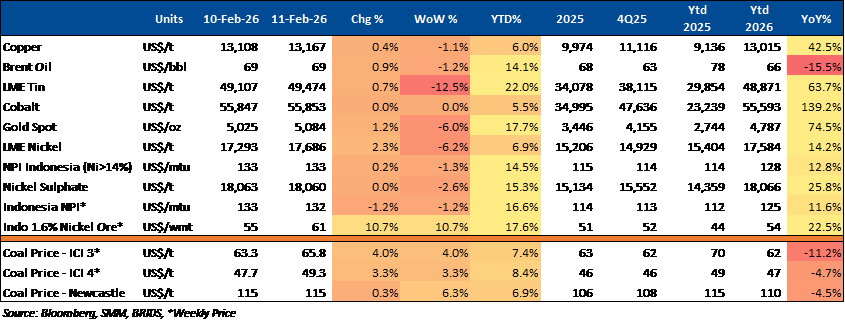

Commodity Price Daily Update Feb 11, 2026

Indonesian Government to Enforce 30% Coal DMO for PKP2B and State Miners

The Energy Ministry will impose a 30% coal Domestic Market Obligation (DMO) on first-generation PKP2B miners and state-owned companies, mainly to secure PLN’s power supply. The policy applies as these miners receive full RKAB approval, with the DMO price for PLN unchanged at US$70/ton. The DMO ratio is higher than 2025’s 23–24%, while total coal production remains around 600 million tons per year. (Kontan)

IBC Targets EV Battery Recycling Industry by 2029–2030

IBC plans to develop an EV battery recycling industry by 2029–2030, focusing on nickel-based used batteries as a secondary raw material source. The initiative aims to support Indonesia’s battery supply chain and circular economy, although challenges remain in investment needs, supply certainty, infrastructure, and regulatory support. (Kontan)

CORPORATE

MEDC Secures Cendramas PSC Operatorship in Malaysia

MEDC, through Medco Asia Pacific Limited, received an appointment from PETRONAS to operate the Cendramas Production Sharing Contract (PSC) in Malaysia, alongside partners DIALOG Resources and EnQuest. The project reflects MEDC’s regional expansion and is subject to final PSC and joint operating agreement requirements. (Emiten News)