|

FROM EQUITY RESEARCH DESK |

|

||||||||||||||

|

IDEA OF THE DAY |

|

|

|

|

|

|

|||||||||

|

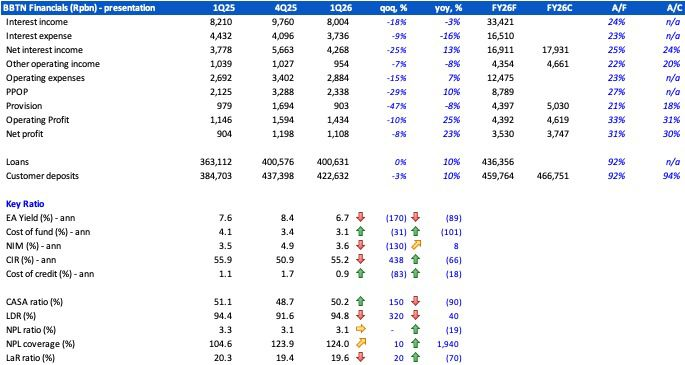

RESEARCH COMMENTARY BBTN (Buy, TP: Rp1,500) - 1Q26 Results: Above 1Q26 Insights: · Solid start to FY26 with 23% NP growth: BBTN posted 1Q26 net profit of Rp1.1tr (-8% qoq, +23% yoy), accounting for 31% of our FY26F and 30% of consensus, above. · NII softened qoq as NIM normalised from a high base: NIM came in at 3.6% (+8bps yoy, but down 130bps qoq from 4Q25’s elevated base). The qoq decline mainly reflected lower EA yield after the strong 4Q25 base, although management reiterated plans to push more high-yield loans beyond mortgages to support yields going forward. · EA yield declined but CoF continued to improve on better deposit mix: EA yield declined to 6.7% (-170bps qoq, -89bps yoy), while CoF improved further to 3.1% (-31bps qoq, -101bps yoy). Management attributed this to tighter CoF monitoring, repricing down expensive deposits, limiting special-rate approvals, and continuing to shift from high-cost to low-cost CASA. · CASA improved sequentially: CASA ratio rose to 50.2% (+150bps qoq), although still down 90bps yoy. Management noted low-cost CASA had increased by around Rp20tr over the past year, supported by stronger digital transaction activity, while high-cost CASA was deliberately reduced. · Provisioning fell sharply, supporting earnings resilience: Provision expenses fell to Rp903bn (-47% qoq, -8% yoy), bringing CoC down to 0.9% (-83bps, -18bps yoy). This was supported by better booking quality and stronger collections, helped by underwriting centralisation, collection-model changes, and greater use of analytics and geotagging. · Asset quality remained stable: NPL ratio was flat qoq at 3.1% and improved 19bps yoy, while NPL coverage rose to 124.0% (+10bps qoq, +1,940bps yoy). · Loan growth remained solid: Loans were broadly flat qoq at Rp400.6tr (+10% yoy), while deposits stood at Rp422.6tr (-3% qoq, +10% yoy), bringing LDR to 94.8%. Management stated that BBTN is being more selective in non-subsidised mortgages and is shifting from developer-led growth toward a direct-to-consumer approach via payroll partnerships and institutional ecosystems to create demand.

FY26 Guidance: · Loan growth: 8-10% yoy (10.3% yoy) · Deposit Growth: 7-9% (9.9% yoy) · NPL: < 3.0% (1Q26: 3.1%) · CoC: 1.0-1.2% (1Q26: 0.9%) · NPL Coverage: 125-130% (1Q26: 124%)

Summary: · In our view, BBTN's 1Q26 results were solid, with earnings supported by lower CoC and continued improvement in CoF, despite margin normalisation from the strong 4Q25 base. BBTN’s earnings are increasingly being supported by structural improvements in funding, underwriting, collections, and digital transaction engines.

MARKET NEWS |

|||||||||||||||

MACROECONOMY

US Treasury Yields Edged Higher, with the 10-year Note Rising to 4.27%

US Treasury yields edged higher, with the 10-year note rising to 4.27% after two sessions of declines, though it remained near one-month lows. Markets trimmed geopolitical risk premiums as investors grew hopeful about diplomatic progress between the US and Iran and softer oil prices. President Donald Trump said the conflict was close to ending, with further negotiations expected soon. The Federal Reserve is widely seen holding rates steady this year, while Chicago Fed President Austan Goolsbee signaled potential rate cuts could be postponed until 2027 if oil prices stay elevated. (Trading Economics)

SECTOR

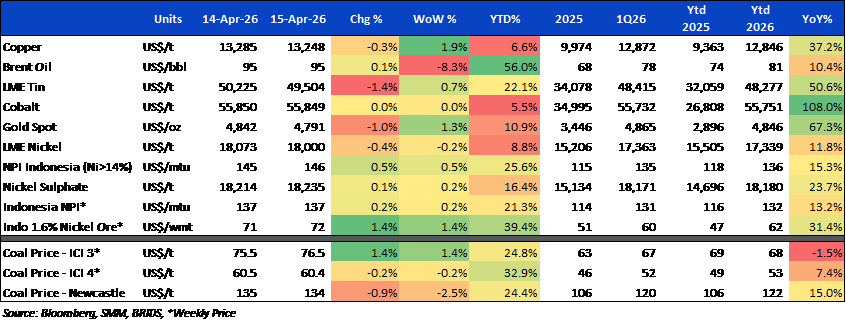

Commodity Price Daily Update Apr 15, 2026

CORPORATE

AALI Declares Rp458 per share Dividend

AALI approved a total FY25 dividend of Rp458 per share (yield: 5.7%), consisting of Rp123 interim and Rp335 final, representing a 60% payout from Rp881.5bn net profit and implying ~5.6% yield. The distribution is supported by solid operational performance, with CPO production rising 6% and sales up 13% in 2025, while the company plans Rp1.4tr capex in 2026 mainly for replanting to sustain long-term output. (Emiten News)

BBNI Plans New AT1 Issuance and Buyback

BBNI plans to issue new offshore AT1 instruments while conducting a buyback of its 2021 AT1 via a tender offer (Apr 14–22, settlement Apr 24) to optimize capital structure and support future growth. (Emiten News)

PGEO Expands into Hydrogen Generator Rental Business

PGEO plans to enter the hydrogen-based generator rental business (HFCG) by adding a new business classification (KBLI 77395), covering equipment provision, installation, operation, and maintenance. The move aligns with its geothermal core and clean energy strategy, with initial targets including Pertamina Group entities. (Bisnis)

To see the full version of this snapshoot, please click here