|

FROM EQUITY RESEARCH DESK |

|

|||||||||||

|

IDEA OF THE DAY |

|

|

|

|

|

|

||||||

|

Retail: 4Q25 Preview: Expansion-Led Growth, SSSG Gradually Recovering (OVERWEIGHT) · We estimate 4Q25/FY25 sector revenue growth of +6.5/+6.5% yoy, relatively in line with our and consensus estimates. · Given the manageable opex, we expect sector op profit to increase by +6.6% yoy in 4Q25 with estimated core profit growth of +4.1% yoy. · Maintain Overweight on the sector; top picks are MIDI (Buy, TP Rp550) and MAPA (Buy, TP Rp800). To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

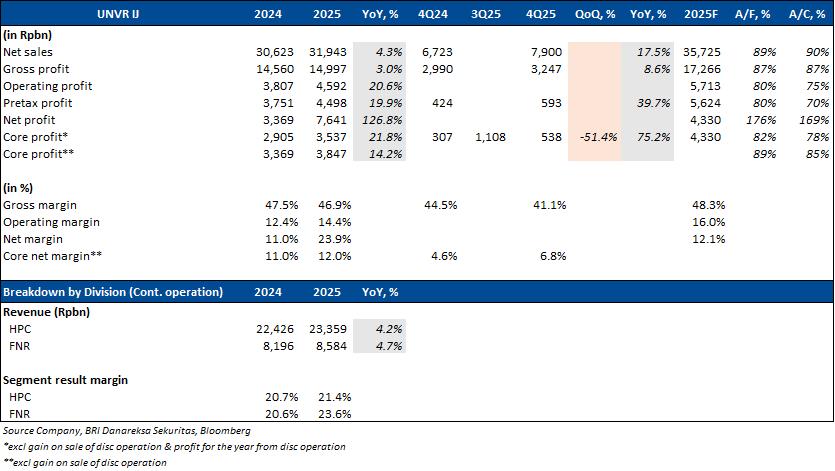

RESEARCH COMMENTARY UNVR (Buy, TP Rp3,200) – 4Q25 Results & Earnings Call Takeaways · UNVR reported FY25 revenue growth of +4.3% yoy, excluding the sales contribution from ice cream and Sariwangi tea – below expectations as ours and cons’ estimates have yet to exclude the contribution from ice cream and Sariwangi. Its net profit jumped 126.8% yoy following the one-off gain from ice cream worth Rp3.8tr and profit from discontinued operations. Meanwhile, core profit excl. one-off divestment gains grew 14.2% yoy with core net margin improving to 12% in FY25F. · Operating profit still grew 20.6% yoy on lower employees’ expenses following the transfer of 700 employees from ice cream business last year. As such, operating margin improved to 14.4% in FY25 from 12.4% in FY24. · In 4Q25, revenue grew 17.5% yoy; its Home & Personal Care (HPC) segment outperformed with domestic sales growth of +20.2% yoy led by volume growth of +13.6% and the remaining +6.6% from higher ASP. On the other hand, Foods & Refreshment (F&R) recorded +4.8% yoy domestic sales growth. Gross margin dropped to 41.1% due to higher transformation costs invested during the quarter. · Going into FY26, the company aims to drive growth ahead of the market with volume to be the growth driver. Additionally, it also targets modest margin improvement coming from 1) sales leverage and 2) cost discipline (they guide transformation cost to be ~30-40% lower compared to last year and further employee cost savings will come from Sariwangi employees). · Special dividend - part of the ice cream dividend has been paid in Dec25, the final tranche will take place in 2Q26. For Sariwangi, management is committed to distribute 100% net gains worth ~Rp800bn. Timing will be further disclosed later. · Management expects 1Q26 growth to be impacted slightly by ~3% due to the Eid timing as both stock-in and stock-out will happen in 1Q26 (last year’s stock-in happened in 1Q25, yet stock-out in 2Q25). (Christy Halim & Sabela Nur Amalina – BRIDS)

MARKET NEWS |

||||||||||||

SECTOR

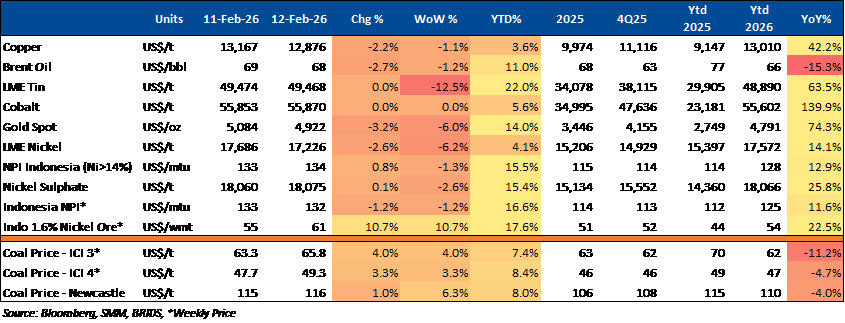

Commodity Price Daily Update Feb 12, 2026

Automotive: Indonesia Car Sales Show YoY Growth in Jan26

GAIKINDO reported car wholesales of 66,447 units (+7.0% yoy/-29.4% mom) in Jan26. Meanwhile, retail sales reached 66,396 units (+4.5% yoy, -28.7% mom). The sharp monthly decline was mainly due to strong year-end 2025 promotions and changes in incentives. Top wholesale sales by brand were Toyota (20,078 units), Daihatsu (12,513 units), Mitsubishi (6,898 units), BYD (4,879 units), and Honda (4,016 units). Despite ongoing macro challenges, GAIKINDO remains optimistic about achieving around 850,000 units in sales in 2026. (Kontan)

CORPORATE

WIFI Partners with Bina Karya to Develop ICT Infrastructure in IKN

WIFI has partnered with state-owned PT Bina Karya (Persero) to support the development of ICT infrastructure in Indonesia’s new capital, Nusantara (IKN), covering fiber optic networks, broadband access, and integrated connectivity systems to accelerate digital ecosystem development. (Bisnis)