Equity Strategy

FY26 Outlook: Still a Stock Picker’s Market Amid Gradual Growth Recovery

- Despite reasonable FY26 earnings expectations, a gradual recovery should continue to favor bottom-up stock picking.

- While we still see upside for conglo/ index stocks, our fundamental view also favors Telco, Metals, Consumers, and Poultry sectors.

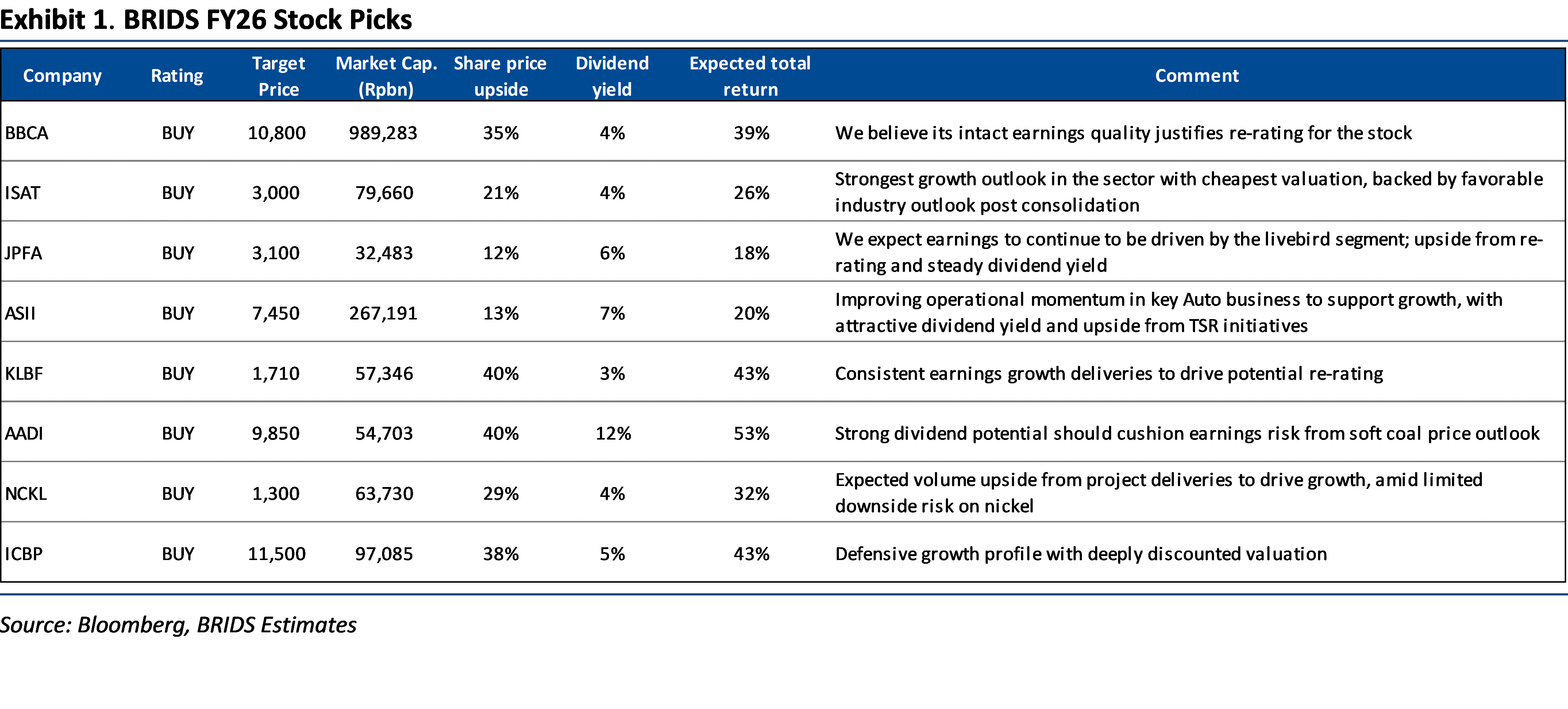

- We set the FY26-end JCI target at 9,440; Our bottom-up total-return screen highlights BBCA, ISAT, JPFA, ASII, KLBF, AADI, NCKL, ICBP as key picks.

A reasonable growth expectation with cushion from dividend

As earnings growth fell short in FY25 (9M25: -7% yoy), our FY26 EPS growth forecast of 8% yoy appears achievable given FY25’s low base. If growth does re-emerge, a combination of undemanding valuations (overall market’s 15x FY26 PE/ 10x PE ex-conglo stocks) and 5% dividend yield, should position Indonesia favorably within EM, particularly if foreign investors look to rotate away from the tech/ AI-driven North Asian markets. Aggregate earnings showed initial signs of bottoming in 3Q25 (+14% qoq/ -1% yoy), but the 3Q seasonal effect means investors may seek further confirmation of recovery in 4Q25-1Q26 before turning more constructive.

Aligned macroeconomic supports to further aid growth recovery

Alongside indication of bottoming earnings, industry data (i.e., retailers’ SSSG, auto sales, and loan growth) also points to early signs of rebound in 3Q25 (Exh.19-22). Unlike early FY25, we see macroeconomic conditions becoming increasingly aligned to support growth recovery into FY26, with the expected acceleration in government fiscal spending, rollout of key govt. programs (MBG’s budget of Rp335tr), including a firm govt social protection budget (+8.6% yoy). That said, the phased rollout of the key programs and still subdued capex spending likely mean that recovery will be gradual.

The shifting landscape: conglo and index flow theme may prevail

JCI’s +23% YTD gain as of 17th Dec25 has lifted market capitalization to Rp15,873tr, with Rp2,432tr of the gains coming from conglo and index-theme stocks (50% YTD increase for the group). With domestic and foreign institutional investors taking larger participation in 2H25, we see scope for this theme to continue into FY26. We estimate a potential 17-32% upside in market cap for the conglo names should this theme persist in FY26.

Sector picks: favoring sectors with better visibility

Given still tentative recovery scenario, FY26 may likely be another year for bottom-up/ stock-picking. Nonetheless, in terms of our sector picks, we stick with selected domestic sectors with better growth visibility.

- Within the domestic sectors, Banks and Consumers are pricing in a subdued FY26 EPS growth outlook (Banks: +4% yoy, Consumers: +6%), reflecting still tepid demand outlook. We believe Telco (FY26 EBITDA growth of 7%), Poultry (FY26 EPS growth of +4%) and Retailers (FY26 EPS growth of +16%) are among sectors with better growth visibility.

- In commodities space, we project Metals sector to have an attractive FY26 EPS growth outlook of 27%. This is largely supported by our expectation of volume growth from new projects and expansion across companies (i.e., BRMS, INCO, MBMA). Given still flattish price outlook for nickel, we expect the FY26 performance to favor those with exposure to gold (BRMS) and tin (TINS). We also expect potential valuation upside from the new assets, such as in the case of DEWA and BRMS.

JCI FY26-end target of 9,440

We set our FY26-end JCI target at 9,440, based on the following assumptions: 1) FY26 EPS growth of 8% and a 14.2x PE multiple, in line with the five-year average for the fundamental stocks group; 2) a 40% premium to reflect continued fund flows for conglomerate and index-aspirant stocks. Our bull and bear case targets of 9,820 and 9,135, respectively, assume 10% and 6% EPS growth. Key market risks include potential overhangs or shifts in government policy and programs, as well as changes to key index methodology.

Stock picks

We screen stocks across key sectors under our coverage based on the highest expected forward total return, and make our final selections based on our assessment of re-rating potential and dividend sustainability. Our top picks are as follows:

… Read More 20251218 Equity Strategy