BRIDS Market Pulse

In the Spotlight

- Market and Sector Performance

JCI fell -2.4% w-w to 6,960, breaching the psychological 7,000 level for the first time since the war began, with YTD losses deepening to -19.5%. This week's decline was led by domestic-facing headwinds rather than war escalation, with broad but more moderate sell off: Heavy Equipment (-8.8%) and Auto/ ASII (-5.5%) on UNTR’s 1Q26 earnings miss, Banks (-2.8%) on continued foreign outflow despite in-line 1Q26 earnings, Retail (-3.9%) and Metals (-2.6%) despite the sectors’ earnings beat, Consumer (-2.4%). Telco (-0.2%) outperformed amid TLKM’s flat w-w. Only four sectors posted positive returns: Cigarettes (+8.0%), Oil & Gas (+3.9%), Industrial Estate (+1.9%) and Coal (+2.8%). Among JCI movers, DSSA (-20.0%) remained the single largest drag for the second consecutive week, followed by BBCA (-3.3%), TPIA (-11.7%), ASII (-5.5%), and BBRI (–2.6%). On the upside, GGRM (+16.8%) led on cigarette excise relief speculation, BUMI (+11.1%), GOTO (+3.8%) on earnings beat, AADI (+6.9%).

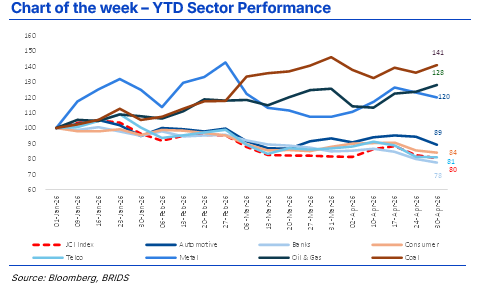

- YTD Sector Scorecard (as of 30 April)

The YTD picture underscores a clear message that the market is rewarding only those sectors with direct commodity upside from the war (coal, O&G, metals) while punishing rate-sensitive (Banks, Property, Tower) and import-exposed (Consumer) sectors. Outperformers are entirely energy and commodity-exposed: Coal (+42.5%), Oil & Gas (+27.4%), and Metal (+10.6%). Industrial Estate (+7.6%) and Cigarettes (+6.3%) are the only domestic sectors in the green. Every other sector is negative YTD, with the worst performers being Cement (-27.8%), Tower (-27.5%), Media (-23.0%), Banks (–20.2%), Consumer (-19.4%), and Telco (-19.0%). Within Banks, BBCA (-27.6% YTD) has been the standout underperformer despite inline 1Q26 earnings. The stock is now trading at sub-3SD of its five-year P/BV mean, entirely driven by the Rp5.4tr three-week foreign outflow and MSCI weight reduction fears. UNVR (-41.0% YTD) is the worst-performing large cap in the BRIDS universe.

- Regional Markets

Global markets were mixed this week, with the war narrative largely in a holding pattern (i.e., no major escalation but no breakthrough either). Thailand (+2.6%) and Korea (+1.9%) led, while S&P (+0.9%), China (+0.8%), Dow Jones (+0.5%), India (+0.3%), Malaysia (+0.1%) posted modest gains. Russia and Taiwan were flat. Hong Kong (-0.8%), Japan (-0.3%), Singapore (–0.2%), and UK (–0.1%) were slightly negative. Philippines (-1.8%) and Indonesia (-2.4%) were the worst performers. JCI's underperformance relative to peers for the third consecutive week confirms that the sell-off is now driven predominantly by Indonesia-specific factors: Rupiah weakness (which reached fresh all-time low on 29 April), policy noise, sovereign rating concerns, and MSCI overhang.

- Foreign Flows

The fifth week of April saw outflows persist, with Indonesia recording a net weekly outflow of US$409mn, a sharp acceleration from US$171mn the prior week. YTD cumulative outflows deepened to US$2.9bn. EM markets saw outflow across the board, with India leading the outflows at US$864mn, followed by South Korea (-US$1,535mn), Brazil (-US$345mn), Vietnam (-US$71mn), and Philippines (-US$30mn). Taiwan (+US$14.8mn) saw marginal inflows. For Indonesia, the outflow side continued to be dominated by big banks: BBCA (-Rp2,059bn), BMRI (-Rp1,660bn), BBRI (-Rp1,002bn), ANTM (-Rp467bn), GOTO (-Rp171bn). BBCA's outflows remain above Rp2tn for the second consecutive week. On the inflow side, flows were concentrated in INCO (+Rp157bn), BBNI (+Rp141bn), EMAS (+Rp135bn), ADRO (+Rp109bn), TAPG (+Rp58bn). The three-week outflow total for BBCA alone is now ~Rp5.4tn, the dominant story in JCI foreign flow dynamics.

- 1Q26 Earnings Wrap

1Q26 reporting season skewed positive across our stock coverage, with 30% beats, 46% in line, and 24% misses.

- Beats:

- Metal Mining was the standout outperformer, with TINS, ANTM, and BRMS all delivering margin expansion driven by higher gold, tin, and nickel ore prices; INCO was the lone slight miss due to a planned Furnace 3 rebuild.

- Retail and Poultry also outperformed, the former lifted by gold-linked plays and minimarket execution, the latter by feed inventory cushioning that absorbed rising corn and SBM costs. On the other end.

- Misses:

- Coal Mining, Heavy Equipment, and Auto/ ASII, as all three sectors were dragged by RKAB approval uncertainty (AADI, UNTR) and one-off charges (UNTR's Rp1.15tr PKH and Supreme Energy hits, which flowed through to ASII).

- In-line:

- Banks, Consumer, Healthcare, Telco, and Property, with NIM compression at banks offset by lower CoF and CoC, consumer margins holding ahead of expected 2Q26 cost pressure, healthcare top-line intact but salary intensity rising, and property's recurring income (malls, hotels, hospitals) carrying the load as development sales normalized from a strong 4Q25 base.

- Standout beats:

- TINS, which delivered net profit of Rp1.5tr (+1,184% yoy, 48% of FY26F), driven by both volume recovery (refined tin sales +112.8% yoy) and a 51.5% yoy ASP uplift, the cleanest commodity beat of the season.

- CPIN was the other notable upside surprise, posting record quarterly earnings of Rp2.6tr (+68% yoy, 41% of FY26F) as the 4Q25 feed inventory build-up paid off in margin protection.

- GOTO crossed a fundamental inflection, posting its first-ever net profit (Rp258bn), with adj. EBITDA beating on the back of GTF loan book expansion.

- HRTA also stood out with revenue +197% yoy on domestic wholesale strength to bullion institutions.

- Standout misses:

- UNTR delivered just 4% of FY26F net profit (Rp643bn, -80% yoy) due to Rp1.15tr in one-off charges plus the absence of Martabe contribution; ASII missed by extension.

- AADI missed at 11% of FY26F as conservative production stance amid RKAB uncertainty was compounded by higher overburden removal lifting unit costs.

- HEAL missed (18% of consensus) on rising salary intensity (30.7% of revenue), and PWON missed (16% of consensus) despite resilient recurring income, due to below-the-line pressure.

- FY26 guidance: the dominant message from sector guidance is caution around 2Q26 macro pressures.

- Across Consumers (MYOR, UNVR), Middle East tensions are flagged as the trigger for cost pass-through emerging from 2Q26 onwards; UNVR explicitly plans price adjustments on oil-linked SKUs from June 2026, while MYOR has built a 23–25% gross margin range and ~30% packaging cost increase into its FY26 assumptions.

- Banks struck a similar note: BBRI sensitivity-tested asset quality at oil US$100–130/bbl (net NPL could rise from 1.7% to 2–3%, CoC up 35–75bps); BNGA and others may add macro buffers in 2Q26. BBNI held FY26 guidance unchanged (8–10% loan growth, NIM 3.5–3.8%, CoC 1.0–1.2%).

- For the resources complex, recovery is conditional: AADI expects production and OB normalization from 2Q26; UNTR targets Martabe restart by end-May/early-June and TTA RKAB revision by May (15Mt vs approved 7.5Mt); BRMS reiterates ~80koz FY26 gold target with stronger 2H26 delivery post-pushback; INCO's full year under 82% payability supports a stronger revenue base.

- GOTO maintained its Rp3.2–3.4tr FY26 EBITDA guidance and signaled accelerated buyback execution on the remaining US$86mn.

Overall, consensus guidance risk appears tilted to the downside for 2Q26 across consumer and banking earnings as cost pass-through and provisioning catch up to commodity inflation, while the upside lies in resources names where regulatory and operational normalization should reverse the 1Q26 drag.

… Read More 202600504 BRIDSMarketPulse