BRIDS Market Pulse

In the Spotlight

- Market and Sector Performance

JCI rose +2.4% w-w to 7,634 as of 17 April, narrowing YTD losses to –11.7%. The rally was driven by a rotation into commodity and cyclical plays, as the war narrative shifted from ceasefire optimism to active Hormuz resolution. Top performing sectors were Oil & Gas (+8.0%), Coal (+5.9%), and Metal (+5.5%). In contrast, Banks (–1.6%) and Telco (–2.4%). underperformed. Among JCI movers, conglo stocks: BREN (+14.2%), BRPT (+16.4%), MORA, DSSA, and ANTM were the top positive contributors, while the fundamentals group stocks remain the drag with BBCA (–4.1%), followed by TLKM and BMRI.

- Regional Markets

Global markets were broadly positive during the week, led by Korea (+5.7%), S&P (+4.5%), Taiwan (+3.9%), and Dow Jones (+3.2%), reflecting risk-on sentiment as the Hormuz situation evolved toward resolution. Japan (+2.7%) and Indonesia (+2.4%) posted solid gains, while China (+1.6%), India (+1.2%), and Hong Kong (+1.0%) were more muted.

- Foreign Funds Flow

The third week of April saw Indonesia record a net weekly outflow of US$158mn, reversing the US$194mn inflow of the prior week, with YTD cumulative outflows deepening to US$2.4bn. Regionally, EM flows were mixed: India saw modest inflows of US$352mn, while Taiwan led with US$5.1bn of inflows and South Korea US$130mn. Brazil saw significant outflows of US$565mn. The commodity rotation theme continued to dominate and was clearly visible on the inflow side: EMAS, ASII, MEDC, AADI and INCO. However, bank outflows persisted heavily: BBRI, BBCA, and BMRI were the three largest outflows. The persistent bank selling (BBRI and BBCA each seeing ~Rp1tn of weekly outflows) remains the dominant drag on aggregate flow numbers and index upside.

- War Watch: Hormuz Reopens, But Fragility Remains. Another dramatic week of developments:

- US naval blockade (13 April): Following the failed Islamabad talks, Trump declared a US naval blockade of the Strait of Hormuz targeting all ships entering or leaving Iranian ports. The US military confirmed the blockade was "fully implemented" by mid-week, having turned back 10 ships. Iran's armed forces threatened to block all shipping from the Persian Gulf, Sea of Oman, and Red Sea if the US continued its blockade.

- Hormuz reopened (17 April): In the week's most significant development, Iran's FM Araghchi announced on 17 April that the Strait of Hormuz is fully open to all commercial shipping traffic during the truce in Lebanon.

- Ceasefire expiry: The two-week ceasefire is set to expire on 22 April. The White House said conversations are "productive and ongoing".

- Indonesia Policy Response

- Pertamina raised non-subsidized fuel prices effective 18 April, with steep increases on premium grades, while Pertamax (RON 92) was held unchanged at Rp12,300 and Pertalite remains at Rp10,000. The move signals that the government's strategy of absorbing the oil shock through the budget has reached its limit on the non-subsidized segment, where Pertamina can no longer hold prices given the gap to global market levels. With Hormuz now declared open and oil prices pulling back sharply (~11% on the day), the fiscal pressure from energy subsidies should ease if the reopening holds, though the non-subsidized hike suggests the damage to Pertamina's margins has already been done.

- The nickel HPM revision and new royalty rates under PP 19/2025 (14–19%) take effect 26 April.

- ANTM (Buy, TP Rp4,800) – FY26 Outlook: Higher cost and levy risks offset by stronger nickel ore and gold volume. ANTM secured ~18.1mn wmt of Ni ore for FY26 RKAB , supporting higher nickel ore volume. We also expect gold sales to recover. We see limited risk on export levy implementation, as ANTM’s exposure is mainly on FeNi (~2% of total revenue). We maintain Buy rating with unchanged TP of Rp4,800, supported by resilient nickel ore economics and improving gold segment FY26F.

- MEDC (Buy, TP raised to Rp2,200) – FY26F earnings rebound prospect on higher volumes, AMMN and oil tailwinds. MEDC’s FY25 headline earnings was weak, but its core operations stayed resilient, with 4Q25 O&G production rose to 176 mboepd. We expect FY26F earnings to improve on Corridor, Forel and Terubuk contribution, plus higher oil assumption amid ME tensions. We maintain Buy rating and raise TP to Rp2,200, backed by 42-44% FY26F-27F earnings upgrades and stronger AMMN support.

- HRTA (Buy, TP raised to Rp3,300) – Riding the gold bullion upcycle; Resuming coverage with Buy Rating and TP of Rp3,300. HRTA is a key beneficiary of the shift to investment-driven gold demand, with gold bars now dominating 87.6% of sales & MS rising to a record 69.9% in FY25. We project solid FY26F revenue growth of +57.6% yoy, driven by higher gold bars volumes & higher gold price and expect margins to be broadly stable. We resume coverage with a Buy rating and TP Rp3,300 based on 10x FY26F PE. Currently, HRTA still trades attractively at 8.3x FY26F PE.

- Week Ahead: Key Catalysts (18–24 Apr 2026)

- Ceasefire expiry (22 April): The two-week ceasefire expires. Any breakdown could reverse the Hormuz reopening and send oil sharply higher.

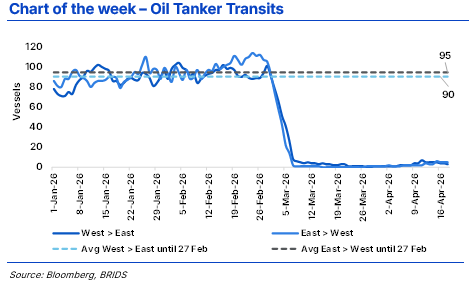

- Hormuz normalization: Watch for tanker throughput data: pre-war was 130–160 ships/day. Even with Iran's declaration, mine clearance and insurance reinstatement will take time.

- Bank Indonesia RDG (21-22 April): Consensus expects BI to hold rate at 4.75%.

- Conglo stocks: After two weeks of outperformance, the market will watch for news on MSCI and IDX reform to potentially impact sentiment on the conglo stocks and JCI’s recovery.

- The week was defined by the Hormuz reopening on 17 April:

- Brent crude traded around US$97–100/bbl for most of the week as the US blockade maintained supply pressure. On 17 April, Iran's announcement that Hormuz is fully open sent prices plunging ~11%, with Brent dropping sharply toward US$87–90/bbl. If the reopening holds and tanker traffic normalizes, further downside is possible over the coming weeks, though the 230+ tanker backlog and mine clearance requirements will slow normalization.

- Gold advanced to US$4,830/oz (+1.7% w-w) as the market priced in a higher probability of a lasting peace deal.

- Thermal coal: ICI-3 (GAR 5,000) edged up to US$77.4/t (from US$76.5 last week), while ICI-4 (GAR 4,200) ticked up slightly to US$60.7/t (from US$60.4). The ICI-3/ICI-4 spread continues to widen, consistent with ongoing gas-to-coal switching across North Asia favoring higher-CV grades for power generation substitution. Newcastle futures pulled back to US$134.0/t (from US$140.5), likely reflecting the initial Hormuz reopening impact on LNG flow expectations.

- Base metals rallied on improved risk appetite: LME nickel and copper firmed during the week.

… Read More 20260420 BRIDSMarketPulse