BRIDS Market Pulse

In the spotlight

- JCI major correction and foreign outflow post MSCI comment

- JCI posted a -6.9% w-w correction alongside US$831mn of foreign outflows following MSCI’s latest statement on Indonesia. Selling pressure was most visible in index-aspirant names (IMPC, BUMI, MORA), followed by several MSCI-heavy / large-liquid names (BREN, BRMS, BBCA, DSSA). On the other hand, GOTO outperformed on domestic and foreign buying amid renewed merger speculation, while metal/gold names (AMMN, EMAS) also held up on continued metals momentum (before the sharp pullback into the weekend).

- Foreign outflows were concentrated in large-cap MSCI constituents, notably BBCA, BMRI, BBRI, and TLKM, consistent with a broader de-risking in liquid proxies. Inflows were more mixed in select conglo names (BRPT, BREN, BRMS) and metal-linked names (AMMN, INCO, NCKL), suggesting investors remain selective even within high beta names.

- Near-term outlook: Policy response and tactical view

- In response to the MSCI review and the leadership shake-up, OJK appointed Friderica Widyasari Dewi and Hasan Fawzi as interim members of its Board of Commissioners to ensure regulatory continuity, while IDX named Jeffrey Hendrik as Acting President Director, who is scheduled to represent the exchange in a meeting with MSCI executives on Monday, 2 Feb26. The government also flagged further policy support to broaden domestic institutional participation, including allowing pension and insurance funds to raise equity market exposure to 20% (from 8%), alongside broader market-structure initiatives around free-float and governance/ transparency improvements.

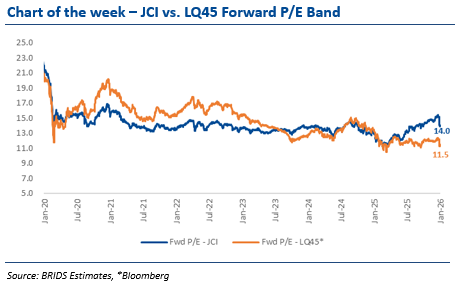

- In our 29 Jan report, we viewed that the market would likely remain in a de-risking mode amid uncertainty around foreign flows. Nonetheless, we believe the latest coordinated response from the government and IDX, together with reports of commitments from Danantara to support market stability, could help improve sentiment at the margin, particularly for large-cap, high-liquidity names (LQ45) amid potential rise in institutional allocation.

- On the flow front, we note that foreign selling pressure appeared to ease into Thursday and Friday, potentially indicating that the initial wave of MSCI-driven de-risking may be moderating.

- Against this backdrop, we see scope for a tactical risk-on rebound as policy support and regulatory follow-through help stabilize sentiment after the initial MSCI-driven de-risking. With foreign selling showing early signs of moderation and domestic institutional participation potentially increasing, we would look to selectively re-engage in our top-pick liquid names (Banks: BBCA, BBNI; Consumers: ICBP; Telco: TLKM, Auto: ASII), which offer both flow support and fundamental resilience.

- BBCA FY25 results: BBCA booked NP of Rp14.1tr in 4Q25, bringing its FY25 NP to Rp57.5tr (+5% yoy), slightly above our estimate and in line with consensus. Management expects a higher loan growth of 8-10%, lower NIM of 5.45.6%, stable CoC of 40-50bps, and improving consolidated CIR at 31-33%. We maintain our BUY recommendation with a higher TP of Rp11,400 taking into account the higher FY26F ROE as we adjusted FY26 earnings by +5% from lower opex.

- Commodities:

- Metals: Metals markets saw sharp volatility into the weekend, with gold and silver correcting from record highs and copper easing off peak levels, highlighting an increasingly positioning-driven commodity tape. The reversal appeared to be driven largely by profit-taking and margin-related liquidation following an outsized January rally, compounded by thinner late-week liquidity conditions. Copper’s pullback similarly reflected a near-term reset in speculative positioning after its sharp run-up on tight-supply optimism. Overall, near-term metals price action remains sensitive to liquidity and positioning dynamics, even as the medium-term structural backdrop stays broadly supportive.

- Coal: Indonesian coal prices continued to rise (ICI3: US$63.3/t; 2.1% w-w, ICI4: US$47.7/t; 0.8% w-w), in-line with increases in China’s domestic prices ahead of the upcoming new year holiday. Unconfirmed reports indicated 34% cut in Indonesia’s coal production quota.

… Read More 20260202 BRIDSMarketPulse