BRIDS Market Pulse

In the spotlight

- Commodities theme continued to support JCI outperformance

- JCI rose ~2.2% wow, outperforming several regional peers amid a continuation of commodity-driven rally. Metals (+10.7%) and Oil & Gas (+7.3%) were the top-performing sectors, supported by sharp moves in nickel, copper, and energy prices during the week. This more than offset weakness in Telco (-6.8%), Property (-1.8%), and Banks (-0.8%), where valuation support remains insufficient to drive near-term rerating. The divergence reinforces our view of limited earnings growth visibility for the domestic sectors in 1Q26.

- Stock gains were concentrated in resource and high-beta names, with market leadership was driven by AMMN (+19.9%), MDKA (+15.9%), INCO (+18.9%), ANTM (+13.1%), BYAN (+5.4%), and BUMI (+10.0%), reflecting continued strong momentum chasing in resource names. In contrast, declines in CUAN (-12.2%), IMPC (-9.7%), COIN (-15.5%), TPIA (-5.6%), and BMRI (-4.3%) capped broader index upside.

- Foreign investors posted net inflows into Indonesia in the first week of Jan26, marking the 14 consecutive week of inflow, standing out against persistent outflows in India and Taiwan, while flows remained selective toward South Korea and Brazil. Largest inflows were booked in ANTM, BBRI, ASII, and BBCA, alongside commodity-linked names such as INCO and MDKA. Notably, inflows into BBCA and BBRI suggest selective re-entry into large-cap banks. On the other hand, heavy outflows from BUMI, BMRI, CUAN point to de-risking in crowded, high-beta index stocks, underscoring that foreign participation remains selective rather than index-wide.

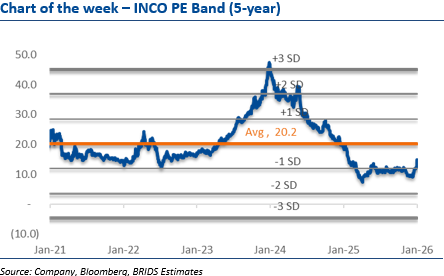

- INCO (Buy, TP raised to Rp6,800) – Potential beneficiary of higher nickel price as ore monetization plan is on track. We see emerging scenario of nickel price upside amid potential 34% cut in Indonesia’s FY26 RKAB, which we estimate could swing global refined nickel balance from +107kt surplus to ~0.7–1.0Mt deficit. We raise our nickel price assumption to US$17–17.5k/t (vs. US$16–16.5k/t previously), lifting INCO’s FY26–27 earnings outlook despite conservative volume assumptions. INCO’s ore monetization plan remains on track, though we conservatively assume 14.5mn wmt ore sales in FY26–27 (vs. mgmt target 20mn wmt) to factor in RKAB timing risk. Our analyst Andhika Audrey resume coverage with Buy rating and raise our TP to Rp6,800 (prev. Rp4,700), implying FY27F PE ~13x.

- Telco (OW): Fixed broadband race kicks off. We project FBB penetration could reach ~41% in FY26, underpinned by 1.4GHz FWA, challenger-led price disruption, and open-access FiberCos. The rising competition and open-access fiber pose downside risk to MNO FBB ARPU, while mobile momentum continues to anchor core earnings. We see WIFI and INET to offer growth exposure at 12.4x/18.9x 26F EV/EBITDA, underpinned by strong cons. EBITDA growth of ~2.2x/~12.0x in 2026F. ISAT (Buy, TP Rp3,000 remains our sector top pick).

- Consumers (OW): Decent Dec25 sales indication; Wage hike and fiscal tailwinds support intact The FY26 national avg min wage hike of +5.7% yoy should provide support to consumption despite it being slightly lower than FY25. Our sector FY26 EPS growth outlook of 8.6% remains underpinned by the expectation of a more expansionary and flexible fiscal policy. Our top pick remains ICBP (Buy, TP Rp11,500), followed by MYOR (Buy, TP Rp2,700).

- Commodities: Copper climbed ~+2.3% w-w, supported by tightening supply outlook and expected stronger physical demand signals. Nickel surged ~+4.8% w-w, driven by anticipation of supply tightness from Indonesia’s policy. Gold also edged higher by ~+1.5% w-w, helped by continued safe-haven demand amid lingering macro uncertainties. Indonesian thermal coal price rose slightly amid resumption of China restocking.

… Read More 20260112 BRIDSMarketPulse