BRIDS Market Pulse

In the spotlight

- Another big correction week for JCI, but foreign fund outflows eased

- JCI posted a second consecutive week of sharp correction, down -4.7% w-w, putting the market as the worst performer within EM YTD (-8.2% YTD). The week’s correction was led by the conglo-related/ ex-index aspirant names (DSSA -13.8% w-w, MORA -52.5%, FILM -55.3% w-w, BREN -5.9%) and metal plays, with TLKM the only fundamental names seeing a sharp correction on the back of market talks of a potential accelerated asset depreciation. Investors’ rotation into fundamental names drove outperformances in Consumers (+7.2% w-w), Cigarettes (+6.4%), Auto (5.5%) and Banks (+2.6%) though the momentum was slowed by the news on Moody’s outlook revision at the end of the week.

- Foreign funds flows: Following large US$831mn outflow induced by MSCI’s statement in the previous week, outflow moderated to US$68mn, with the week’s selling dominated by the metal names. Flows in the large-cap fundamental names were mixed with inflows into BBCA, BMRI and ASII, and outflows into BBNI, BBRI, TLKM.

- Domestic fund Jan26 positioning:

- Based on Jan26 KSEI data, domestic fund shifted back into Banks (+86bps add, BMRI and BBNI were largest adds), reflecting flight to quality amid the expected market weakness following MSCI’s review into May26. Funds also added Metals (+203bps, largest addition in ANTM, TINS) and Coal (+50bps, largely in ADRO and AADI). Reduced positioning were Auto/ ASII (-67bps) and Heavy equipment/ UNTR (-25bps), driven by news on possible revocation of Martabe mine’s contract.

- Foreign investors’ ownership fell further to 41% (ex-corporate) with notable cut in ownership in BBCA and GOTO, following news of MSCI review. Foreign investors maintained ownerships in other large-cap banks, and blue-chip names ASII, TLKM as well as the metal names.

- Moody’s sovereign outlook revision: We believe the outlook revision should be seen as an early signal of higher risk premium rather than a credit event. While the move may drive near-term caution toward Indonesian assets, it should not trigger forced selling or structural repricing. As such, we expect the equity market impact to be incremental to risk-off sentiment already reflected in recent foreign fund outflows (US$711mn YTD) from the JCI. A limited foreign inflow of US$55.9mn on Friday supported this view.

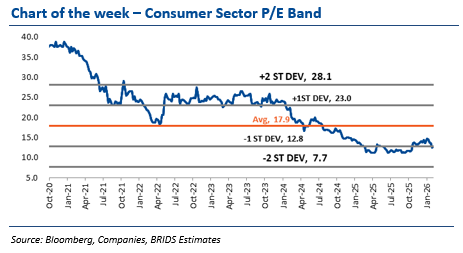

- Consumers: 4Q25 preview. Analyst Christy Halim published a timely preview amid renewed interest on the sector from the foreign and domestic funds. We estimate 4Q25/ FY25 sector revenue growth of +6.7/+4.2% yoy, broadly in line with consensus’ est. of +4.1% yoy. The revenue growth is mainly supported by ICBP and MYOR, while we also expect GPM recovery in 4Q25 on normalization in soft commodity prices. We reiterate our Overweight stance on the sector; ICBP (Buy, TP Rp11,500) remains the top pick in the sector.

- BBNI (Buy, TP Rp4,700): in-line 4Q25 results: robust NIM allowed room for proactive provisioning in 4Q25. BBNI booked FY25 net profit of Rp20.0tr (–7% yoy), meeting our estimate but slightly below (98% of FY25F) consensus as CoC spiked in 4Q25. CoF and NIM improved materially in 4Q25 but management expects a conservative NIM for FY26F at 3.5-3.8% vs FY25’s 3.8%. We maintain Buy rating with an unchanged TP of Rp4,700.

- BMRI (Buy, TP Rp5,500): Record-high quarterly profit in 4Q25. BMRI posted a net profit of Rp18.6tr in 4Q25 (+40% qoq, +35% yoy), driven by resilient NIM, strong non-interest income, contained opex, and minimal CoC. Supported by the strong 4Q25, BMRI recorded a net profit of Rp56.3tr (+1% yoy) in FY25, above our and consensus estimates (114%/ 110% of FY25F).

- MEDC (Buy, TP Rp2,000): Higher Corridor ownership and AMMN normalization to support FY26 earnings. Analyst Andhika Audrey resumes coverage with Buy rating and higher TP of Rp2,000. We expect AMMN to drive 4Q25F and FY26 earnings rebound despite oil price pressure, supported by copper export approval. We expect the Corridor PSC ownership increase to drive FY26F production uplift, contributing ~30% of estimated total production vol. We upgraded FY26F-27F earnings and raise our TP to Rp2,000, reflecting higher output assumptions and rerating supported by AMMN recovery.

- INET (Not Rated): In transition phase toward monetization. Analyst Kafi Ananta take on INET’s strategy and plan: NET expands to B2C FTTH, FTTH contracting, and IRU Submarine with the main driver to be B2C FTTH supported by a targeted 2.8mn HP rollout. The Rp4.2tr capital raising and acquisitions will support this expansion, with management indicating that further acquisitions may be pursued. Earnings ramp-up is expected from FY27F as the FTTH rollout begins; dependency on a single ecosystem remains a key risk. Based on consensus forecast, INET currently trades at 15.1x/9.4x FY26F/FY27F EV/EBITDA, which we view as fair for an ISP/ FiberCo.

- Commodities:

- Metals: Metals prices were volatile over the week, with gold correcting from recent highs after an extended rally, reflecting profit-taking and positioning normalization despite continued safe-haven support. Similar volatility is also shown in copper, underscoring near-term metals direction remains largely flow- and liquidity-driven even as medium-term structural demand themes remain intact. Nickel remained relatively resilient, supported by supply-discipline expectations around Indonesian production and constructive sentiment in stainless-steel demand.

- Coal: Indonesian thermal coal prices maintained positive momentum with ICI3 and ICI4 at US$65.8/t (+4.0% w-w) and US$49.3/t (+3.3% w-w). The thermal coal market continued to digest potential supply cut from Indonesia, amid speculation on RKAB numbers. Our check with the coal miners indicated that the numbers are yet to be official.

… Read More 20260209 BRIDSMarketPulse