BRIDS Market Pulse

In the Spotlight

- Market and Sector Performance

JCI corrected -6.6% w-w to 7,131 as of 24 April, the worst weekly decline since the war began, as Rupiah weakness and the ceasefire extension failed to calm markets and triggered a broad risk-off, deepening YTD losses to -17.5%. The sell-off was indiscriminate with Banks (-5.0% w-w), Telco (-8.1%), Consumer (-6.9%), Metals (-15.3%), and Coal (-2.5%). The largest drag was driven by the conglo stocks, which led the prior two weeks' rally, reflecting reversal in DSSA (-37.8%) and BREN (-30.3%), as the market priced in MSCI exclusion risk.

- Regional Markets

Global markets were broadly negative this week, though the damage was concentrated in net energy importers and EM, consistent with the worsening war narrative rather than a broad risk-off. Brent surged ~18% w-w to ~US$106/bbl, though VIX notably remained contained, settling at ~19 this week. The S&P (+0.5%) hitting all-time highs while VIX stayed subdued suggests US equity markets are largely shrugging off the Hormuz disruption. JCI (-6.6%) was the worst performer in the region by a wide margin, followed by the India (-2.3%), and Thailand (-1.8%). Philippines (-0.9%), Hong Kong (-0.7%), posted smaller losses. The North Asian markets continued to diverge on structural AI/semiconductor demand.

- Rupiah and MSCI

Beyond the war, two Indonesia-specific catalysts amplified the sell-off. First, the rupiah breached Rp17,300/USD on 23 April, a historic low approaching the 1998 crisis nadir. BI Governor acknowledged the rupiah is "undervalued" and does not reflect fundamentals. Second, MSCI on 20 April announced it would maintain its freeze on Indonesia's index rebalancing for the May 2026 review and extend its full assessment to June. MSCI stated it would remove stocks flagged under Indonesia's new High Shareholding Concentration (HSC) framework, and may use the more granular >1% shareholder data to revise free float estimates downward. This means: no new stock additions, no FIF or NOS increases, and potential exclusions of concentrated names.

- Foreign Flows

The fourth week of April saw a sharp acceleration in outflows, with Indonesia recording a net weekly outflow of US$171mn, deepening YTD cumulative outflows to US$2.5bn. Regionally, EM flows were broadly negative: India saw the largest outflows at US$278mn, followed by Thailand (-US$222mn), Vietnam (-US$199mn), Philippines (-US$41mn), and Brazil (–US$565mn), while Taiwan (+US$4.1bn) diverged. In Exhibit 4, JCI’s outflow was dominated by big banks and conglo reversal, with BBCA and BBRI each seeing their heaviest weekly outflows of the year. BBCA's Rp2.4tn outflow in a single week is particularly notable and likely reflects both risk-off positioning and pre-emptive selling ahead of MSCI rebalancing. The flow picture is increasingly alarming as both banks and conglos are now seeing heavy outflows simultaneously, removing the rotation dynamic that had supported the index in prior weeks.

- War Watch: Ceasefire Extended, But Hormuz Attack Continued

- The ceasefire, set to expire on 22 April, was extended by Trump indefinitely to give Iran time to present a "unified proposal" at Pakistan's request. However, the extension was immediately undermined:

- Iran reimposed "strict control" over Hormuz on 19 April, reversing its 17 April declaration that the strait was fully open, citing the ongoing US naval blockade as a ceasefire violation. Hormuz traffic collapsed to just ~12 vessels/day (vs. 130–160 pre-war).

- Trump gave Iran 3–5 days (by ~25–27 April) to engage in negotiations before resuming attacks.

- Indonesia Policy Response

Bank Indonesia held its benchmark rate at 4.75% at the 21–22 April RDG, as unanimously expected. Governor Perry reiterated that the decision prioritizes external stability and rupiah defense amid war-driven capital outflows. BI also signaled suportive liquidity measures, targeting double-digit base money growth and continuing bond purchases to support domestic liquidity.

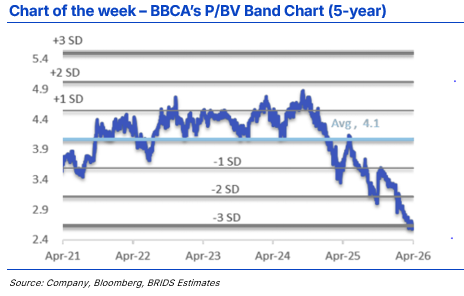

- BBCA (Buy, TP lowered to Rp10,900) – Inline 1Q26 Earnings. BBCA booked a net profit of Rp14.7tr in 1Q26 (+4% qoq, +4% yoy), forming 24% of our and consensus’ FY26F estimates, i.e., in line. Excluding corporate, other segments saw higher qoq NPL and LaR ratios, but still improved yoy driven by wholesale segments. We maintain Buy rating with a lower TP of Rp1 0,900; valuations are attractive at sub -3SD of its five-year mean, but risk remains on foreign outflow ahead of the MSCI rebalancing.

- BMRI (Buy, TP Rp6,200) – 1Q26 Earnings beat on loan expansion and resilient asset quality. BMRI posted a net profit of Rp15.4tr in 1Q26, (-17% qoq, +17% yoy forming 27% of our and consensus’ FY26 estimates, i.e., above). The bank delivered a solid top line and lower CoC were driven by the expansion of related-party loan which grew 56% while retail loans remain weak. We maintain Buy rating with an unchanged TP of Rp6,200 implying a fair value PBV of 1.8x and 8.3% dividend yield.

- WIFI (Buy, TP raised to Rp4,500) – Solid FTTH execution; FWA is key driver for the next leg. WIFI’s FTTH execution remained on track, with 2.5mn home-passes and 1.5mn home-connect achieved, driving Rp541bn FY25 FTTH revenue. FWA rollout to drive 26F growth with our projection of 2.3mn subs; Mgmt. indicated potential bond refinancing to support capex plan. We maintain Buy with a higher TP of Rp4,500; current valuation is attractive at 9.5x/4.0x FY26/27F EV/EBITDA.

- Commodities

- Brent crude surged ~18% w-w as Iran reimposed Hormuz controls on 19 April and attacked ships on 22 April, reversing the prior week's oil price decline. The Brent spot-futures spread blew out to a US$25/bbl premium (per EIA), reflecting extreme short-term market tightness from the Hormuz disruption.

- Gold reversed course this week, falling ~3% w-w to ~US$4,700/oz (from ~US$4,830 last week) amid continued inverse oil-gold dynamic (i.e, elevated oil price pushes out rate cut expectations, despite the geopolitical risk premium). A potential resumption of peace talks provided some support into the close at ~US$4,710.

- Base metals LME nickel rallied sharply to ~US$19,125/t (+6–7% w-w), supported by tightening supply expectations, and the implementation of PP 19/2025 royalty revision which raises Indonesia's upstream cost floor (see our report). However, LME copper was broadly flat as the global risk-off and dollar strength capped gains.

- Thermal coal: ICI-3 (GAR 5,000) edged up slightly to US$77.7/t (from US$77.4 last week), while ICI-4 (GAR 4,200) held flat at US$60.7/t. Newcastle futures steady at US$134.0/t. In China, domestic thermal coal prices were largely firm during the week, but offseason demand is capping upside as the market is in the spring shoulder season between winter heating and summer cooling peaks. Port inventories at northern China ports remain high at ~2,347kt, above the five-year average, which limits pricing power for seaborne coal. The import window for Indonesian coal is reopening as domestic prices firm, but high port stocks and selective downstream buying temper enthusiasm. The ICI-3/ICI-4 spread (now ~US$17/t) remains wide, consistent with ongoing gas-to-coal switching across North Asia favoring higher-CV grades This is in-line with our channel check with AADI this week.

- JCI Reform

MSCI on 20 April maintained its freeze on Indonesia's index rebalancing for the May 2026 review. Two separate reviews are now in play: 1) the MSCI Semi-Annual Index Review (announcement 12 May, effective 1 June), where BREN and DSSA are widely expected to be removed as the only two MSCI constituents on the HSC list, and MSCI may also use >1% shareholder data to revise free float estimates downward for other constituents; and 2) the MSCI Market Accessibility Review, expected in June, which will determine whether Indonesia's reform progress is sufficient to lift the current freeze. The near-term impact is negative, with Indonesia's weight in the MSCI EM index is likely to decline in the May review, and the June accessibility review introduces a further overhang.

- Week Ahead: Key Catalyst

- Iran 3–5 day deadline (~25–27 April): Trump gave Iran a short window to engage in negotiations or face resumed attacks. Reports suggest Iranian FM Araghchi may travel to Islamabad, raising cautious hopes of a breakthrough, though no formal negotiations are confirmed.

- FOMC meeting (28–29 April): The Fed is expected to hold at 3.50–3.75%, but commentary on oil/inflation impact and the Fed chair transition (Powell's term ending, Warsh nomination) will be closely watched.

- 1Q26 earnings due out on April 30th. Thus far, large Banks have reported in-line earnings and improving growth in 1Q26 amid resilient loan growth and NIM, though management guidance started to reflect a more conservative BI rate outlook.

- IDX LQ45/IDX30/IDX80 rebalancing. IDX announced results on 24 April, effective 4 May (first trading day of May). Key changes:

- LQ45: CUAN, DEWA, ESSA, HRTA, WIFI in; BREN, CTRA, DSSA, HEAL, NCKL out

- IDX30: ADMR in, ISAT out

- IDX80: BKSL, CBDK, DEWA, GGRM, TPIA in; BREN, BTPS, DSSA, MTEL, NCKL out

This is the first evaluation incorporating HSC criteria, with BREN and DSSA removed from all three indices, aligning with MSCI's expected exclusion.

… Read More 20260427 BRIDS Market Pulse