BRIDS Market Pulse

In the Spotlight

- Market and Sector Performance

JCI recorded its sharpest weekly gain of 2026, rising approximately 7.4% w-w to close at ~6,008 on Friday (Jun 12), the first weekly gain in eight consecutive weeks. Monday (Jun 8) opened on the back foot with the index falling ~2.9% intraday as the rupiah weakened beyond Rp18,100/USD. The inflection came following BI Governor and Finance Minister Purbaya joint press conference on the previous weekend, committing to increase the attractiveness of Indonesian asset yields and enhance fiscal-monetary coordination. This was followed by BI's surprise +25bps rate hike to 5.50% on Tuesday Jun 9, the first inter-meeting move in eight years, which triggered a 7.57% single-session JCI surge. Positive catalysts continued to accumulate through the week: Danantara COO Dony Oskaria clarified on Jun 8 that DSI will not take profit margins and will only charge service fees, materially reducing the "state trader" discount on commodity exporters; the government signalled an upward revision to RKAB mining quotas; and war narratives turned constructive.

On BRIDS coverage, all sectors closed positive w-w with one exception. Best performers: Banks (+10.8%), Coal (+7.3%), Property (+5.9%), Heavy Equipment (+5.9%), Metal (+5.3%), Pharmaceuticals (+5.2%). Relative laggards: Infrastructure (-7.5%, entirely JSMR), Cigarettes (-2.0%), Poultry (-2.2%), Technology (-0.3%). The biggest positive index contributors were large-cap banks: BBCA (+16.7%), BBNI (+10.9%), BMRI (+9.4%), BRIS (+5.9%), BBRI (+4.0%); while AADI (+14.2%) and HRUM (+15.4%) led coal on RKAB revision signals. TPIA (+41.8%) was the week's standout.

The week's moves validated the directional thrust of our prior strategy note, though the EY-bond spread, while having compressed from peak of ~325bps, has not yet normalized to pre-selloff levels.

Despite the rebound's scale, risk remains at the forefront with several upcoming events: BI's Jun 17-18 scheduled meeting, MSCI Market Accessibility review on Jun 18, S&P outlook review (end of June/ early July), and review on DSI operational execution. On the global market, investors will closely watch the upcoming FOMC meeting and resolution of peace deal.

- Foreign Flows

Foreign investors remained net sellers during the week, though at a materially moderated pace versus the prior week's broad institutional de-risking. Indonesia recorded a WTD outflow of US$334mn (Exhibit 2), a significant deceleration from recent weeks. JCI’s rebound was driven by domestic players as local institutions and retail absorbed selling pressure in large caps. YTD cumulative equity outflows stand at US$3,898.2mn, still among the more severe in the region in absolute terms, though Indonesia's YTD outflow is modest relative to India (-US$30.2bn) and South Korea (-US$78.2bn).

Regionally, the WTD selling was broad and concentrated in North Asia: South Korea (-US$2.3bn) and Taiwan (-US$8.5bn) dominated outflows, likely reflecting tech-sector rotation and global risk-off episodic selling. The Philippines was the only market to record a marginal inflow this week (+US$1.9mn). On a YTD basis, Brazil remains the standout positive outlier in the EM universe (+US$7.1bn), while Thailand (+US$800mn YTD) continues to attract modest inflows.

- Indonesia Policy and Macro Watch

The week marked a visible shift in policy communication tone. The Jun 7 joint BI-MoF press conference carried symbolic weight as the first coordinated public signal from both institutions.

BI's off cycle +25bps hike to 5.50% on Jun 9, the first inter-meeting move in eight years, bringing cumulative tightening to 75bps over three weeks, was framed explicitly as a "pro-stability" measure. The rupiah responded, strengthening from Rp18,100+ to close at Rp17,860/USD by Friday, still weak in absolute terms but a meaningful stabilization signal. Another hike at the Jun 17-18 scheduled meeting cannot be ruled out.

On DSI, the COO's Jun 8 clarification that DSI will charge only service fees and will not function as a commodity trader materially reduced the negative reading the market had priced in recent weeks. The revised framework positions DSI as a price-monitoring and compliance body through the transition period, with full digital platform rollout targeted for January 2027. The worst-case "state trader" scenario might have been largely ruled out, though implementation uncertainty through the transition period remains.

On RKAB, the government signalled an upward revision to mining quotas, a meaningful policy reversal from the deep cuts (coal target ~600mt vs 2025's 790mt realisation; nickel ore at 260-270mt vs 379mt) that had forced shutdowns and squeezed downstream margins. This is the more immediately actionable positive for coal and nickel names alongside the DSI clarification, and explains much of the outperformance in AADI, HRUM, NCKL, and INCO this week.

On budget, government’s indication of budget efficiency should reaffirm the Rp67tr MBG reduction, signalling that fiscal consolidation is being maintained heading into the S&P July review window. The World Bank revised Indonesia's 2026 GDP growth forecast to 5.0% on Jun 11.

- War Watch

The Iran-US conflict shifted decisively from an escalation to a deal-imminent narrative this week, a significant positive for EM oil-importer sentiment broadly and Indonesia specifically. On Jun 11, Iranian forces briefly halted a tanker from transiting Hormuz; on Jun 12, US forces shot down two Iranian drones targeting commercial vessels. Both incidents were contained without escalating into the direct strike exchanges that characterized the prior week. On the same day, Pakistan's PM Sharif announced a "final, agreed text" had been reached, Iran's FM Araghchi stated a deal had "never been closer," and Trump indicated a potential signing as early as Jun 14, with a White House official citing 80% probability. Key reported deal parameters include reopening of the Strait of Hormuz, dismantling of Iran's nuclear program, removal of the US naval blockade, and economic reconstruction incentives.

- Key Research Reports

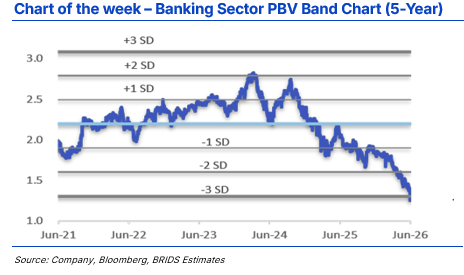

- Banks (Upgrade to Overweight; BBCA top pick)

We upgraded the banking sector to Overweight from Neutral, as the 15-36% YTD share price decline has pushed valuations well past fundamentals (i.e., current PBV at >-3SD of the 5-year mean implies earnings contractions of -22.8% for BBRI, -14.9% for BBCA, -12.7% for BMRI, and -11.1% for BBNI, which we view as excessive). BBCA is our top pick given superior ROA without leverage expansion and the strongest CASA franchise to defend margins in a rising rate environment; BTPS is our second preference on low leverage and already-elevated CoC. On NIM, we expect funding costs to reprice faster than lending yields given wholesale depositor concentration, putting BBRI, BMRI, and BBNI at greater risk of compression. Foreign positioning remains light, as of 2Q26 bank sector outflows through Jun 9 stand at Rp29,996bn, led by BBCA (-Rp12,668bn), BMRI (-Rp8,557bn), and BBRI (-Rp8,499bn). We expect this to amplify upside on any sentiment reversal. Key downside risks: asset quality deterioration and higher-than-expected NIM compression.

- Metal Mining (Overweight maintained; ANTM and TINS top picks)

We see regulatory risks for the sector moderating, as ESDM Minister Bahlil confirmed the gross-split scheme will remain exclusive to oil & gas (removing a key mining overhang), signalled a more flexible price-linked RKAB approach, and deferred the royalty revision pending a revised formula. The one remaining structural overhang is Permendag 17/2026, which from Jan 1, 2027 channels ferroalloy exports through PT DSI. We view sector’s exposure as sharply differentiated across names. NCKL bears the heaviest direct impact, with ~76% of revenue (Rp22.5tr) from NPI exports falling squarely under HS 7202.60 (ferronickel) and routed to Lygend and Glencore on payment-against-documents terms. MBMA sits at the opposite end with all NPI sold domestically within IMIP and its sole export (nickel matte, HS 7501) outside DSI scope entirely. INCO is likewise structurally insulated via nickel

matte and prospective MHP exports. We prefer: 1) ANTM (Buy, TP Rp4,800) as ferronickel exports represent only ~2.5% of revenue, with the top line dominated by royalty-free domestic gold trading, and RKAB additions should support 2H26 volumes. 2) TINS (Buy, TP Rp4,500), which has zero DSI exposure as tin sits entirely outside the three covered commodities, with structural demand from solder and semiconductors intact.

- Commodities

- Brent crude fell sharply to approximately US$87-88/bbl by Friday close, down roughly 6-8% w-w from last week's ~US$93-95/bbl, the largest weekly decline in months, as growing peace deal optimism drove a significant unwind of the conflict risk premium. Despite this, Brent remains well above pre-conflict levels, and full relief is contingent on Hormuz reopening in practice.

- Thermal coal was broadly stable w-w. Newcastle futures ~US$145/t (flat), ICI-3 c.US$86/t, ICI-4 c.US$67/t. China port inventory at c.2,321kt, above both the 2025 trajectory and 5-year seasonal average, suggesting limited near-term demand-driven upside in seaborne prices. The more material development for Indonesian coal names this week was the RKAB upward revision signal rather than the spot price movement.

- Precious metals: Gold fell sharply mid-week, breaching US$4,200 and hitting an intraday low of around US$4,10/oz level on Wednesday Jun 10, the lowest since September 2023 and the first breach of the 200-day moving average, before partially recovering to close Friday near US$4,216/oz. The structural central bank accumulation narrative remains intact but is being overshadowed near-term by the global rate-higher environment. Silver followed gold lower.

- Base metals: LME copper held near US$14,040/t (3-month), supported by structural supply constraints. LME nickel recovered modestly, with Indonesia's RKAB upward revision providing an additional supply-side supportive signal alongside declining LME inventories. LME tin stable with no fresh directional catalyst.

- Week Ahead: Key Catalysts

- MSCI Global Market Accessibility review.

- BI Board of Governors scheduled meeting Jun 17-18, market will watch for further rate action, with possible hike not to be ruled out.

- FTSE rebalancing.

- FOMC Meeting to be chaired for the first time by Kevin Warsh.

- Iran-US deal signing confirmation and Strait of Hormuz reopening timeline.

- S&P sovereign outlook review window (end of Jun/ early July); watch for any pre-announcement signals.

… Read More 20260615 BRIDS Market Pulse