|

FROM EQUITY RESEARCH DESK |

|

|||||||||||

|

IDEA OF THE DAY |

|

|

|

|

|

|

||||||

|

GOTO Gojek Tokopedia: 1Q26 Earnings: First Net Profit Achieved, EBITDA Beat, But Guidance Held on Macro Risks (GOTO.IJ Rp53; BUY TP Rp80) · GOTO posted its first net profit (Rp258bn) in 1Q26, supported by loan book growth to Rp9.9tr, while ODS GTV rose a modest 4% yoy. · Guidance maintained at Rp3.2–3.4tr FY26F EBITDA; potential cost pass-through flagged under fuel price risks. · Maintained Buy rating (TP: Rp80); Buyback pace to accelerate on strong FCF generation and cash position. To see the full version of this report, please click here

BRIDS FIRST TAKE · Aneka Tambang: 1Q26 Earnings: ASP-Led Margin Expansion Drove a Strong Beat, Despite In-Line Volume (ANTM.IJ Rp4,040; BUY TP Rp4,200) To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

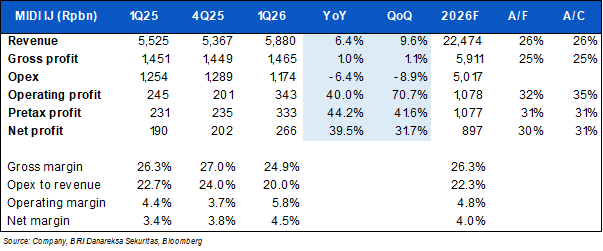

RESEARCH COMMENTARY MIDI (Buy, TP Rp500) – 1Q26 Results: In Line Revenue, Earnings Beat on Lower Opex · MIDI booked 1Q26 rev of Rp5.9tr (+6.4% yoy, +9.6% qoq) – in line with our & cons’ est. Non-food contributed the highest growth of +10% yoy followed by food’s +9.6% yoy, meanwhile fresh food declined by 9.7% yoy. · By geographic, ex-Java continued to drive the growth with its revenue grew +21.9% yoy in 1Q26, while Java ex-Jabodetabek posted flattish growth and Jabodetabek fell by 10.3% yoy. · Cost of rev increased 8.4% yoy in 1Q26 which resulted to 140bps yoy lower gross margin to 24.9%. · Nonetheless, opex-to-revenue declined to 20% in 1Q26 (vs. 1Q25: 22.7%) mainly on lower salary & allowances and depreciation expenses, driving op profit growth of +40% yoy. · Hence, 1Q26 net profit grew strongly at +39.5% yoy and +31.7% yoy to Rp266bn – slightly above ours/cons’ est. at 30/31% of FY26F. And net margin stood at 4.5%. (Christy Halim & Sabela Amalina – BRIDS)

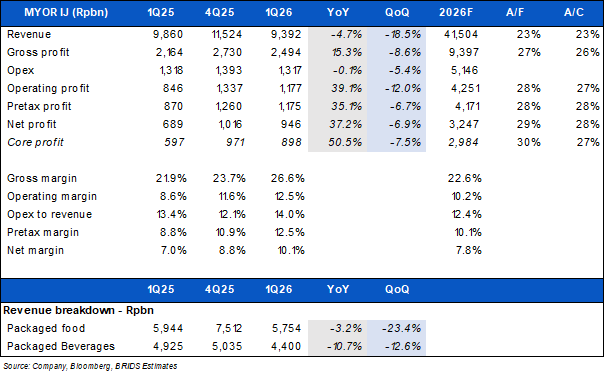

MYOR (Buy, TP Rp2,700) – 1Q26 Results: Soft Rev, Profit Beats on Lower Costs · In line with our preview, MYOR’s rev declined 4.7% yoy (-18.5% qoq) in 1Q26 – relatively in line as part of the domestic sales linked to pre-Eid shifted into 4Q25. · Both product categories posted negative growth where food declined 3.2% yoy meanwhile beverages fell further by -10.7% yoy. · Despite weaker rev growth, net profit rose +37.2% yoy (-6.9% qoq) in 1Q26 – slightly above at 29% of our FY26F, mainly supported by lower raw mat, packaging and flat opex growth. · Both raw mat and packaging costs were 8.8% lower yoy as the impact from Middle East tensions will begin to fully materialize in 2Q26 onwards. Hence, gross margin jumped to 26.6% in 1Q26 – the highest since 1Q24. · With flat opex, op margin also improved to 12.5% with net margin stood at 10.1% in 1Q26. (Christy Halim & Sabela Amalina – BRIDS)

MARKET NEWS |

||||||||||||

MACROECONOMY

|

Bank of Japan Maintained Its Benchmark Rate at 0.75% The Bank of Japan maintained its benchmark rate at 0.75% in a contentious 6-3 vote, the widest split under Governor Kazuo Ueda. While the "stand-pat" decision met market expectations, the dissenting voices fueled a hawkish shift, pushing the yen toward 159/USD. Revised forecasts now project fiscal inflation at 2.8%, while growth estimates were trimmed to 0.5%. Crucially, the BOJ updated its guidance to allow for hikes based on economic "developments" rather than just "improvements." Markets now price in a 74% probability of a rate increase at the June 16 meeting. (Bank of Japan)

Indonesian Government Grants Temporary 0% Import Duty on LPG and Plastics The Indonesian government will temporarily set import duties to 0% for LPG and selected plastic products for six months starting May 2026, aiming to ease cost pressures amid rising global prices. The policy removes the existing 5% LPG tariff and expands eligible plastic products, with the Coordinating Minister for Economic Affairs noting the measure is primarily aimed at supporting the petrochemical sector, which is facing challenges in securing naphtha supply due to ongoing Middle East tensions. (Bloomberg) |

SECTOR

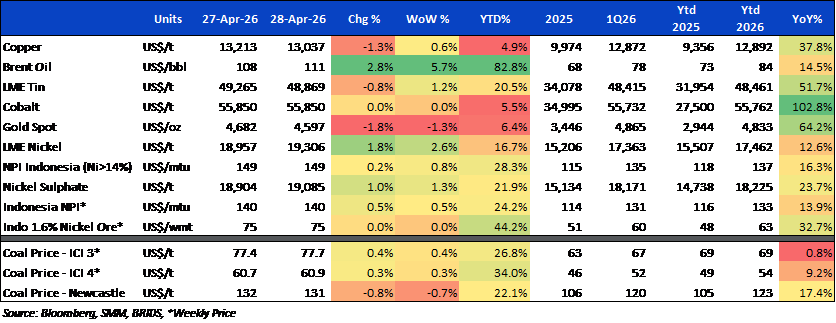

Commodity Price Daily Update Apr 28 , 2026

CORPORATE

CDIA Takes 49% Stake in PSS via US$15.5mn Capital Injection

CDIA will inject US$15.5mn (approximately Rp267bn) into Petrosea Services Solutions Pte. Ltd. (PSS) through the subscription of 9.94mn new shares. Upon completion, CDIA will hold a 49% stake in PSS, while the remaining 51% will be retained by Petrosea Energi dan Infrastruktur Pte. Ltd. (PEPC), a subsidiary of PTRO. The capital injection aims to strengthen PSS’s capital structure and support future business expansion, including working capital needs, operational capacity enhancement, and both organic and inorganic growth initiatives. Bisnis)

Pertamina, PTPN III, and MEDC Partner to Accelerate Bioethanol E20 Target

PT Pertamina, through Pertamina New & Renewable Energy (PNRE), has signed three MoUs with PT Perkebunan Nusantara III (PTPN III) and MEDC (via PT Medco Intidinamika) to support the bioethanol E20 mandate by 2028. The collaboration covers revitalization of a multi-feedstock bioethanol plant in Lampung, development of a new bioethanol plant in Bone, South Sulawesi, and construction of a molasses-based bioethanol facility in partnership with PT Sinergi Gula Nusantara (SGN), a subsidiary of PTPN III. (Kontan)