|

FROM EQUITY RESEARCH DESK |

|

|||||||||||

|

IDEA OF THE DAY |

|

|

|

|

|

|

||||||

|

Poultry: FY26 Outlook: A Prime Time to Harvest · After FY25F’s high base, we expect moderate earnings growth for FY26F due to conservative chicken price assumptions and elevated feed costs. · Higher GPS import quota will lead to excessive supply in FY27-28F, but FY26F supply-demand dynamic will be more favorable than FY25F. · Maintain Overweight rating, with early accumulation to reap the benefits of favorable supply-demand, Eid festive, and harvest season. To see the full version of this report, please click here

Macro Strategy: The Currency Conundrum · IDR remains weak despite foreign inflows, driven by fiscal concerns, DXY rebound, and limited BI excess rupiah liquidity absorption. · Fed signals January rate hold as growth remains solid, labor cools, and easing potential points to later 2026. · US tariff uncertainty persists, but Indonesia remains largely insulated; adverse rulings may pressure USD, potentially easing pressure on IDR. To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

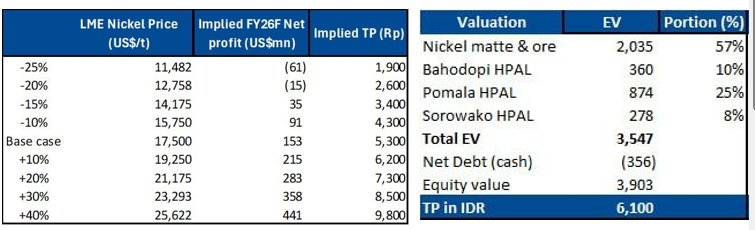

RESEARCH COMMENTARY INCO (Buy, TP Rp6,800) – 2026 RKAB Approved, But Volume Undisclosed · INCO stated that ESDM has approved the company’s 2026 RKAB , allowing the company to resume mining activities at Sorowako, Pomalaa, and Bahodopi. However, the amount of the quota remains undisclosed with the company indicating that:

· FY26 sales volume target: · Mgmt target: ~20mn wmt · Our base-case assumption: 15mn wmt · Despite downside risk in volume, we believe this will be mitigated by potentially higher nickel ore ASP on the back of tightening domestic ore supply following the national production cap. Assuming a scenario where FY26 volume is 50% lower than our base-case, but upside from higher nickel ore prices (assuming ASP of ~US$50/t vs. US$38.5/t in our base case), we see ~18% and ~10% downside on FY26 earnings and our DCF-based TP. · We currently have a Buy rating on INCO with a TP of Rp6,800. (Andhika Audrey & Naura Reyhan Muchlis – BRIDS)

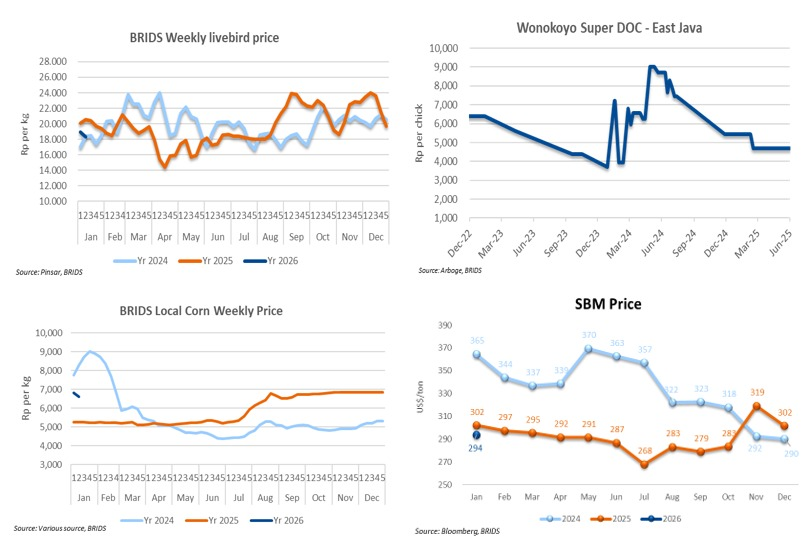

Poultry (Overweight) – 2nd Week of January 2025 Price Update · Livebird prices rebounded to Rp19.3k/kg toward end-week trading. However, the weekly average in the second week of Jan26 declined 3% wow to Rp18.3k/kg. · No official update on DOC, though channel checks suggest prices remained steady at around Rp6.0k/chick. · Local corn prices eased further to Rp6.5k/kg, bringing the weekly average in the second week of Jan26 down 3% wow to Rp6.6k/kg. · SBM prices declined to below US$300/t, pulling the MTD Jan26 average to US$294/t (–3% mom; –3% yoy). · While spot LB prices showed a tentative rebound, the lower weekly average suggests demand recovery remains gradual. Nevertheless, continued easing in corn prices alongside softer SBM costs is providing meaningful cost-side relief, helping to cushion margins amid still-fragile LB price dynamics in early Jan26. (Victor Stefano & Wilastita Sofi – BRIDS)

MARKET NEWS |

||||||||||||

MACROECONOMY

|

China’s GDP Grew 4.5% yoy in 4Q25 China’s GDP grew 4.5% yoy in 4Q25, slightly above expectations but marking the weakest quarterly pace in 2025. Full-year growth reached 5.0% yoy, in line with Beijing’s target, showing resilience amid trade tensions. Domestic demand remained soft despite subsidies, while growth was supported by smaller-than-expected US tariffs, a brief trade truce, and export diversification. (Bloomberg)

China’s Retail Sales Grew 0.9% yoy in Dec25 China’s retail sales grew 0.9% yoy in Dec25, slowing from 1.3% and missing expectations despite ongoing stimulus. This marked the weakest growth since December 2022, reflecting a soft labor market, a prolonged property downturn, and deflationary pressures. Gains in food, clothing, and pharmaceuticals were offset by continued declines in autos, home appliances, and tobacco and alcohol sales. (Trading Economics)

Indonesia’s Manufacturing Sector Strengthened in 4Q25 Indonesia’s manufacturing sector strengthened in 4Q25, remaining in expansion as indicated by the Prompt PMI Bank Indonesia at 51.86%, up from 51.66% in 3Q25. Improvements were driven by higher output, inventories, and total orders, with most subsectors expanding, led by paper products, printing and media reproduction, non-metal mining, and food and beverages. In 1Q26, manufacturing activity is expected to rise further, with PMI-BI projected at 53.17%, supported by stronger orders, production, inventories, and input delivery, particularly in footwear, furniture, metal goods, and food and beverages. (Bank Indonesia) |

SECTOR

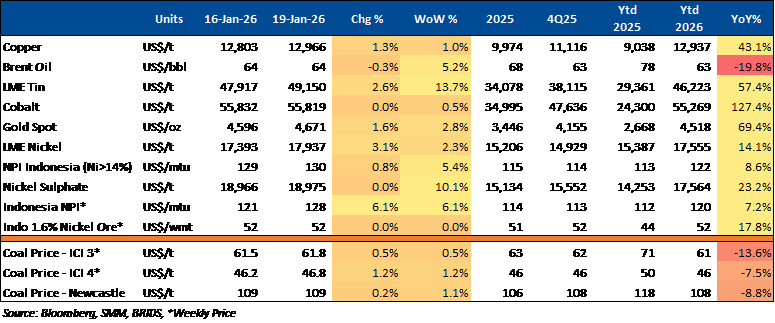

Commodity Price Daily Update Jan 19, 2026

CORPORATE

DEWA Extends Mining Services Contract with Arutmin Worth up to Rp10.5tr

DEWA has extended its mining services contract with PT Arutmin Indonesia for the Asam Asam and Kintap projects in Tanah Laut, South Kalimantan, with an estimated contract value of up to Rp10.5tr. Under the agreement, cumulative overburden removal over the life of the mine is projected to reach around 252 million bcm, while total coal production is estimated at approximately 50 million tons. (Investor Daily)

INDY Establishes New Commercial EV Manufacturing Subsidiary

INDY has established a new subsidiary, PT INVI Manufaktur Andalan Indonesia (IMAI), to engage in the manufacturing of commercial electric vehicles, with business activities covering the production of four-wheeled or higher motor vehicles, vehicle body (karoseri) manufacturing, as well as the manufacturing of trailers and semi-trailers. (Kontan)