|

FROM EQUITY RESEARCH DESK |

|

|||||||||||

|

IDEA OF THE DAY |

|

|

|

|

|

|

||||||

|

Bank BTPS Syariah: 1Q26 Eanings: In Line; Improving Asset Quality Lowers CoC; Sustaining Positive Loan Growth (BTPS.IJ Rp1,005; BUY TP Rp1,400) · BTPS posted a net profit of Rp317bn in 1Q26 (+25% qoq, +3% yoy), forming 24% of our and consensus FY26F estimates, i.e., in line. · Asset quality showed improvement, with CoC declining to a 5-year low of 5.2% amid positive loan growth in the last 2 quarters. · Maintain Buy rating with an unchanged TP of Rp1,400 as we keep our forecast and valuation, implying an FV PBV of 1.0x. To see the full version of this report, please click here

Mayora Indah: Conservative FY26 Top Line Guidance with Managed Margin Resilience (MYOR.IJ Rp1,840; BUY TP Rp2,700) · 1Q26 rev is expected to be flat to slightly down yoy on timing effects of Eid, while margins are expected to remain resilient and potentially improve qoq. · Cost pressures from Middle East tensions to emerge from 2Q26, with modest freight impact and max ~2% margin dilution from packaging cost. · We adjusted FY26/27F net profit estimates by +1.0/-3.3% and reiterate Buy rating, with unchanged TP of Rp2,700. To see the full version of this report, please click here

Macro Strategy: The Next Constraint · IDR weakness reflects external, seasonal, and differential pressures. We shift our pessimistic scenario into the baseline. · BI is stepping up offshore, onshore, and SRBI measures, with rising SRBI yields signaling a tighter liquidity stance. · El Niño and higher fertilizer costs could raise food inflation risks, with pressure likely peaking in early of next year. To see the full version of this report, please click here

To see the full version of this snapshoot, please click here

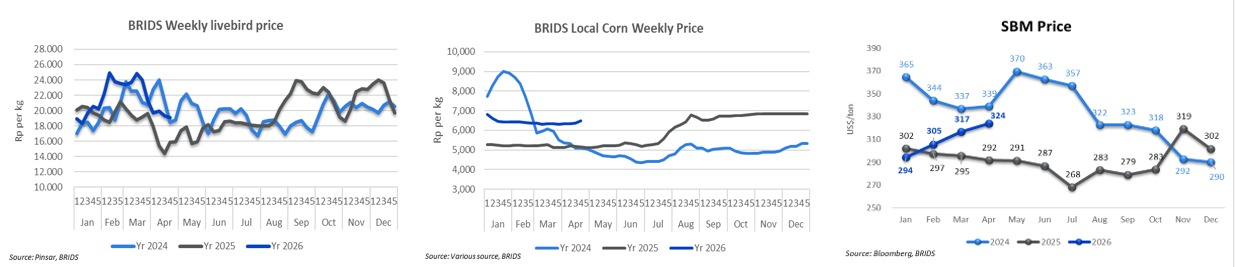

RESEARCH COMMENTARY Poultry (Overweight) – 4th Week of April 2026 Price Update · Livebird prices continued to edge lower to Rp19.3k/kg, dragging the weekly average down to Rp19.1k/kg (–1.2% wow). · Local corn prices ticked up to Rp6.5k/kg, lifting the weekly average by 2.3% wow to Rp6.5k/kg. · SBM prices eased to US$324/t, with the Apr26 MTD average at US$324/t (+2% mom; +11% yoy). · LB prices have continued their downtrend, with prices now hovering below the estimated breakeven level of ~Rp19.6k/kg, indicating growing pressure on integrator margins. While the slight easing in SBM offers some relief, higher corn prices may offset this benefit. Should this trend persist, margins could face near-term pressure, although integrators are still able to capture margins from feed and DOC segments, which should help partially cushion the downside. (Victor Stefano & Wilastita Sofi – BRIDS)

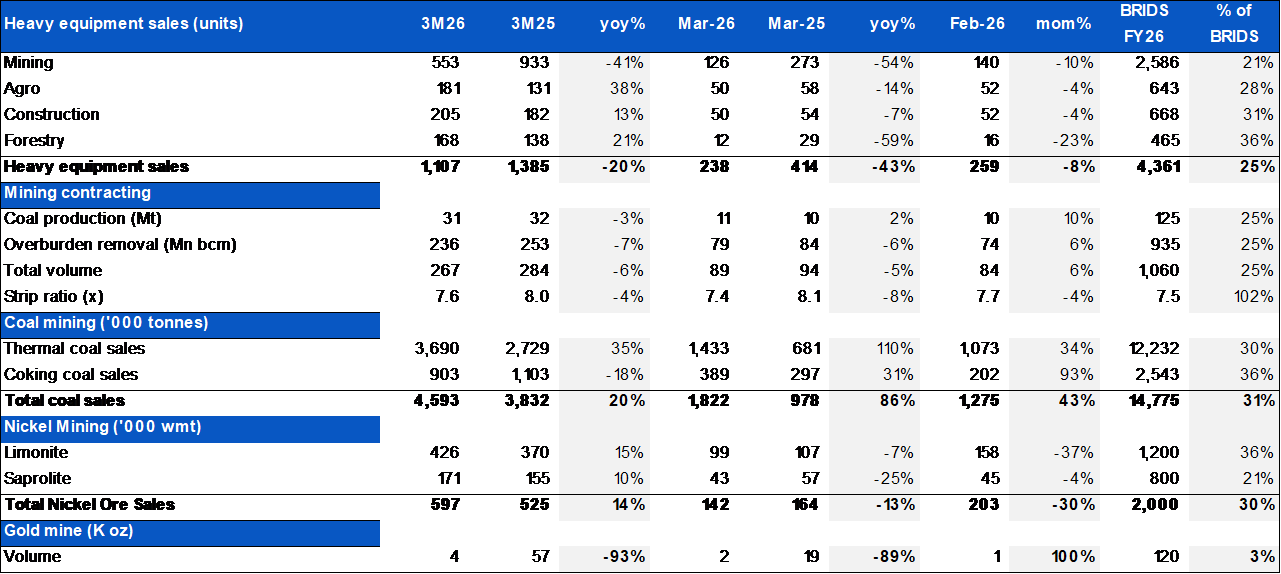

UNTR (BUY, TP Rp32,000) – 1Q26 Operational: Soft yoy, Though Meeting our Conservative Forecast Komatsu sales: · -20% yoy, 25% of FY26F. · Weak sales to Mining segment (-41% yoy) reflected delay of purchases due to RKAB uncertainties. This is offset by stronger sales to Agro and Forestry.

Mining contracting: · Total volumes (Coal+ OB): -4% yoy, 25% of FY26F. · Soft volume also reflected RKAB uncertainty, although 1Q26 volume was still based on 2025 RKAB.

Coal Mining: · The only bright spot +20% yoy, 31% of FY26F.

Gold Mining: · Near zero volume due to absence of contribution from Martabe

Potential implication to earnings (due out on 29th): · Soft sales to mining (big machine) implies potential shortfall on revenue and Pama’s lower volume yoy may weigh on margin given sub-optimum utilization. Additionally, earnings in 2Q26 onwards may also reflect risk from RKAB uncertainty to Pama’s volume, as our check indicates that coal miners will maintain 1Q26 run-rate in 2Q26, but risk if RKAB upward revision is not obtained. (Erindra Krisnawan, CFA & Kafi Ananta – BRIDS)

MARKET NEWS |

||||||||||||

MACROECONOMY

|

Indonesia: Foreign Direct Investment (FDI) into Indonesia Rose 8.5% yoy in 1Q26 Foreign direct investment (FDI) into Indonesia (excluding financial services and oil & gas) rose 8.5% yoy to Rp250tr in 1Q26, extending growth from the previous quarter despite ongoing global uncertainty linked to Middle East tensions. Inflows were led by base metals (US$3.7bn), followed by services and mining. Singapore, Hong Kong, and China remained the main investors. The data reinforce a broader trend of FDI shifting toward downstream mining and refining, supported by Indonesia’s mineral export restrictions in recent years. (BKPM) |

SECTOR

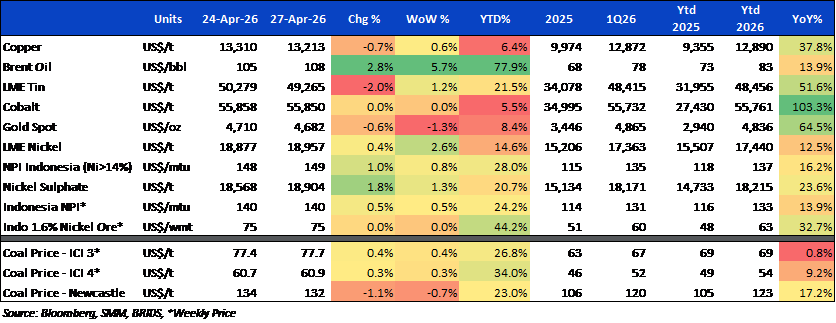

Commodity Price Daily Update Apr 27 , 2026

CORPORATE

AKRA Approves Rp1.98tr Cash Dividend for FY25

AKRA has approved a cash dividend of Rp1.98tr, equivalent to Rp100 per share (6.4% yield), for FY25 at its AGMS. The dividend represents a payout ratio of ~80.1% of the company’s FY25 net profit of Rp2.47tr. (Bisnis)

BUMI Plans Full Acquisition of Loyal Metals for AUD79.1mn

BUMI is advancing its overseas expansion strategy in Australia through a planned 100% acquisition of Loyal Metals Ltd., valued at AUD79.1mn (approximately Rp977bn). Under the Scheme Implementation Deed (SID), Loyal Metals shareholders will receive AUD0.45 per share. The transaction remains subject to shareholder approval and is targeted for completion in Aug26. (Emiten News)